Today, the line between voluntary and mandatory ESG disclosure has blurred. Enterprises are realizing that going beyond compliance isn’t just about reputation. Disclosures, as part of a broader ESG strategy, is a way to enhance key business practices like:

- De-risk regulatory exposure

- Strengthen investor trust

- Showcase social responsibility

- Improve corporate governance

- Boost decision-making org-wide

- Prepare for what comes next

This article explores what’s required versus recommended for various reporting frameworks, who is in scope and when, and why enterprises that embrace voluntary reporting today are the ones that find regulatory compliance easier tomorrow.

What’s required vs. what’s recommended for ESG compliance

The critical distinction between mandatory ESG disclosure and voluntary ESG reporting is accountability.

Mandatory requirements are enforceable by law, often with fines, assurance obligations, and regulatory oversight. Voluntary frameworks are driven by market expectations, stakeholder pressure, and investor demands, but they often set the stage for future regulation.

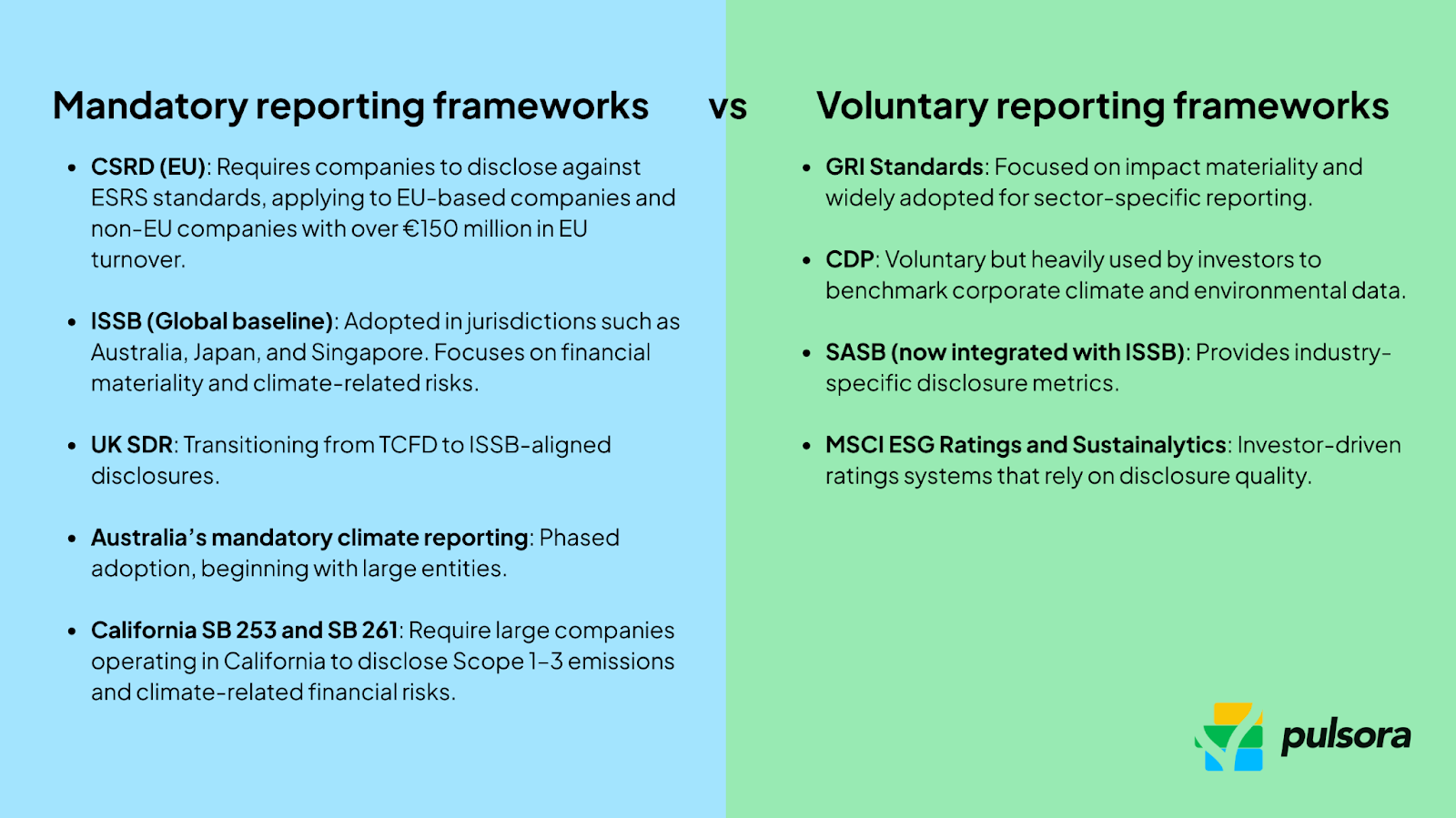

Mandatory frameworks in 2025 include:

- CSRD (EU): Requires companies to disclose against ESRS standards, applying to EU-based companies and non-EU companies with over €150 million in EU turnover.

- ISSB (Global baseline): Adopted in jurisdictions such as Australia, Japan, and Singapore. Focuses on financial materiality and climate-related risks.

- UK SDR: Transitioning from TCFD to ISSB-aligned disclosures.

- Australia’s mandatory climate reporting: Phased adoption, beginning with large entities.

- California SB 253 and SB 261: Require large companies operating in California to disclose Scope 1–3 emissions and climate-related financial risks.

Voluntary frameworks remain influential, including:

- GRI Standards: Focused on impact materiality and widely adopted for sector-specific reporting.

- CDP: Voluntary but heavily used by investors to benchmark corporate climate and environmental data.

- SASB (now integrated with ISSB): Provides industry-specific disclosure metrics.

- MSCI ESG Ratings and Sustainalytics: Investor-driven ratings systems that rely on disclosure quality.

Together, these frameworks show how “voluntary” and “mandatory” increasingly overlap. Many of the metrics companies disclosed voluntarily five years ago are now binding obligations.

Who is in scope and when

For enterprises, scope is determined by size, sector, and geography.

Under CSRD, for example, large EU undertakings are already in scope, and non-EU companies with significant European revenue will follow by 2029. In the U.S., state-level rules apply based on revenue thresholds — $1 billion for California SB 253, $500 million for SB 261. ISSB adoption is more jurisdiction-specific, but in countries like Australia and Japan, large listed companies must begin disclosing from FY 2025 onward.

The deadlines matter because they dictate when companies must begin preparing. For many, reporting obligations begin 12–18 months before the official “first report due” date and often require annual reports every year following. That lead time is essential for conducting double materiality assessments, setting up internal controls, and trialing assurance.

Investors pay close attention not just to whether a company is in scope, but when. They expect proactive preparation of ESG metrics, not last-minute compliance. Enterprises that wait until their first filing deadline risk data gaps, poor audit outcomes, poor financial performance, and damaged credibility.

ESG compliance as a governance and risk function

ESG compliance is a core element of governance and risk management for enterprise-level public companies and private organizations alike.

Mandatory ESG disclosure laws like CSRD and California’s SB 253 treat sustainability data with the same rigor as financial reporting. That means boards and executives are now accountable for ESG compliance in the same way they are for financial statements.

For enterprises, this shift elevates ESG topics from the sustainability team into the boardroom.

Compliance failures expose companies to legal liability, reputational damage, and even exclusion from capital markets. Conversely, robust ESG compliance demonstrates strong governance, effective internal controls, and proactive risk management — qualities investors increasingly reward.

Mandatory ESG disclosure by region

The mandatory ESG disclosure landscape varies by jurisdiction, but the trend is universal: regulators are tightening expectations.

The European Union’s Corporate Sustainability Reporting Directive (CSRD) — guided by the European Sustainability Reporting Standards (ESRS) — has brought double materiality methodology and third-party assurance into law.

Countries from Australia to Japan are adopting the International Sustainability Standards Board (ISSB) standards (IFRS S1 and S2) as their baseline.

In the U.S., the federal climate rule from the Securities and Exchange Commission may have faltered, but California’s SB 253 and SB 261 have pushed mandatory reporting forward at the state level.

At the same time, investors still expect voluntary alignment with global frameworks like the Global Reporting Initiative (GRI), CDP, Sustainability Accounting Standards Board (SASB), and MSCI ESG ratings to provide comparability and context.

In the European Union, CSRD and ESRS set the global benchmark with double materiality, digital tagging, and phased assurance requirements. In the United States, the federal SEC climate rule has faltered, but California’s SB 253 and SB 261 are already shaping ESG compliance for companies with large U.S. operations. The United Kingdom’s Sustainability Disclosure Requirements (SDR) and Australia’s climate disclosure rules are rolling out ISSB-aligned standards from FY 2025 onward. Meanwhile, Japan and Singapore have adopted ISSB principles into listing rules, ensuring that large listed companies disclose climate and sustainability risks in ways comparable to financial statements.

Taken together, these mandates mean large enterprises operating across borders must coordinate ESG compliance strategies globally, ensuring disclosures meet mandatory ESG requirements in multiple jurisdictions simultaneously.

Voluntary vs. mandatory ESG from an investor perspective

For investors, the distinction between voluntary and mandatory ESG disclosure is less important than the quality of the data. They expect companies to meet all mandatory ESG disclosure requirements and then go further, often asking for voluntary alignment with frameworks like GRI, SASB, or CDP to provide additional comparability.

This means that even when companies technically “comply” with the law, investors still value voluntary ESG reporting. It fills gaps left by regulation, especially in areas like biodiversity, just transition, and social safeguards. For asset managers and institutional investors, the most credible companies are those that treat ESG disclosure as part of their core investor communications—not just as compliance paperwork.

Compliance readiness checklist for mandatory and voluntary ESG reporting requirements

Many enterprises underestimate how long ESG compliance takes. Here’s a concise checklist to gauge readiness before your first mandatory filing:

- Governance structure includes clear board-level ESG oversight

- Double materiality assessment completed (for EU CSRD/ESRS)

- Scope 1–3 emissions data mapped, with supplier engagement processes in place

- Internal ESG controls mirror financial reporting controls (audit trails, documentation)

- External assurance provider engaged early, with a dry-run audit completed

- Framework mapping complete (CSRD, ISSB, GRI, CDP) to avoid duplication

- Disclosure calendar aligned with financial reporting cycle

If you can tick these boxes, your enterprise is on the path to reliable, investor-grade ESG compliance.

The future of voluntary vs. mandatory ESG

The current wave of mandatory ESG disclosure has focused on climate and governance, but regulators are already signaling where the next wave will go.

ESG issues like biodiversity, water, circular economy, climate change, and human rights due diligence are all likely to transition from voluntary to mandatory by 2030. The European Commission’s Corporate Sustainability Due Diligence Directive (CSDDD) is one early step in this direction.

Double materiality — currently a uniquely European requirement — is also likely to spread, with stakeholders pushing for impact reporting to match financial risk reporting worldwide. At the same time, digital taxonomies, XBRL tagging, and AI-driven assurance will accelerate the demand for structured, high-quality ESG data.

For enterprises, the lesson is clear: voluntary disclosures today in areas like biodiversity, supply chain transparency, or workforce equity may become tomorrow’s legal requirements. Investing in these systems now ensures smoother compliance later.

Common ESG risks in compliance

As enterprises navigate the shift from voluntary to mandatory ESG disclosure, common pitfalls emerge:

- Underestimating Scope 3 complexity: Supply chain data collection is often the single largest gap in ESG compliance.

- Siloed reporting teams: Treating sustainability and finance as separate functions creates inconsistencies in disclosure.

- Waiting too long for assurance: Engaging auditors only after the first reporting cycle leads to high costs and rework.

- Narrative without data: Reports heavy on storytelling but light on metrics risk being labeled as greenwashing.

- Fragmented frameworks: Without a harmonized strategy, companies duplicate effort across CSRD, ISSB, CDP, and investor questionnaires.

Avoiding these pitfalls requires early preparation, cross-functional governance, and treating ESG compliance as part of the company’s overall enterprise risk management strategy.

Why voluntary now leads to regulatory ease later

Voluntary reporting is not wasted effort; it’s preparation for what regulators will eventually require. Enterprises that align early with frameworks like GRI, CDP, or SASB find themselves at an advantage when mandatory rules arrive.

Voluntary disclosures help companies mature their ESG data systems. They build experience in collecting Scope 3 emissions data, conducting double materiality assessments, and creating governance structures that withstand scrutiny. This reduces the burden when assurance becomes mandatory.

From an investor standpoint, voluntary reporting demonstrates foresight and resilience. It signals that the company is not only compliant with today’s rules but also prepared for tomorrow’s. For customers and supply chain partners, it provides confidence that disclosures are robust and that the company is a reliable long-term partner.

The business benefits of voluntary disclosure

Enterprises that voluntarily disclose beyond compliance see benefits that extend well beyond risk mitigation. Transparent ESG reporting can unlock access to green financing, improve credit ratings, and enhance investor confidence. Many banks and asset managers in the financial markets already integrate ESG factors into lending and investment decisions, which means disclosure quality directly impacts cost of capital.

Voluntary reporting also strengthens supply chain resilience. Large buyers increasingly require supplier ESG disclosures, and early voluntary alignment helps companies maintain and expand business relationships. Internally, the discipline of reporting improves governance, clarifies accountability, and creates stronger alignment between sustainability, finance, and operations teams.

Perhaps most importantly, voluntary disclosure enhances reputation. In a competitive talent market, employees are more likely to join and stay with companies that demonstrate authentic sustainability leadership. In markets where consumers care about sustainability, disclosure builds trust and brand loyalty.

How enterprises can balance voluntary and mandatory ESG disclosure

Enterprises need to strike a balance: mandatory disclosure ensures compliance, but voluntary frameworks help tell the broader story investors and stakeholders want to hear.

A practical approach is to establish a compliance baseline first—mapping requirements across all jurisdictions where the company operates, ensuring that CSRD, ISSB, and state-level rules are fully covered. Once the compliance floor is secure, companies can layer in voluntary frameworks to cover areas not yet mandated, such as biodiversity, water, or human rights.

Integrating voluntary and mandatory frameworks also reduces duplication. For example, aligning CDP responses with CSRD disclosures means a company can satisfy investor expectations while meeting regulatory requirements. Using software platforms to harmonize data across frameworks makes this integration far easier.

Prepare for all kinds of ESG compliance with Pulsora

The difference between voluntary and mandatory ESG reporting is narrowing by the year. What was once optional is rapidly becoming regulated. Enterprises that wait for mandates risk being caught unprepared, while those that embrace voluntary disclosure today position themselves for compliance ease, investor confidence, and long-term enterprise value.

Pulsora helps enterprises manage both voluntary and mandatory ESG disclosures by centralizing sustainability and carbon data, aligning reporting to CSRD, ISSB, GRI, and CDP, and providing audit-ready assurance pathways.

With the right systems in place, enterprises can transform reporting from a compliance burden into a strategic advantage. Book a demo to see how we can help you achieve ESG compliance.

FAQ

Q: What is the difference between voluntary and mandatory ESG reporting?

A: Voluntary ESG reporting is guided by frameworks like GRI or CDP and driven by investor and stakeholder expectations. Mandatory ESG disclosure is set by regulation, such as CSRD or California SB 253, and requires compliance with legal standards, often including assurance.

Q: Which ESG frameworks are mandatory in 2025?

A: Mandatory frameworks include the EU’s CSRD (via ESRS), ISSB adoption in several jurisdictions, the UK SDR, Australia’s mandatory climate reporting, and state-level rules in California.

Q: Do voluntary disclosures help with mandatory ESG compliance?

A: Yes. Voluntary disclosures strengthen data systems, governance, and assurance readiness, making it easier to comply when regulations take effect.

Q: Why do investors still value voluntary ESG reporting?

A: Investors use voluntary disclosures to fill gaps not covered by mandatory frameworks, particularly in areas like biodiversity, Scope 3 emissions, and social impacts. They view voluntary alignment as a sign of leadership and resilience.

Q: How can non-EU companies prepare for CSRD?

A: Non-EU companies with over €150 million in EU turnover must comply by 2029. Preparation includes mapping data systems to ESRS, running double materiality assessments, and building assurance pathways well before the first filing deadline.