The clock is ticking for enterprises when it comes to ESG reporting. 2025 marks a turning point: regulations that were once distant mandates are now hard deadlines. From the EU’s CSRD/ESRS filing requirements, to the ISSB’s global baseline gaining traction, to country-level disclosure regimes in the UK, Japan, and beyond, large companies must not only understand when they are expected to report, but also demonstrate they are “reporting ready” well before those dates arrive.

These deadlines matter because they shape the expectations of regulators, investors, and stakeholders who want timely, comparable, and decision-useful sustainability information. Missing them risks more than non-compliance penalties; it can erode investor confidence, disrupt supplier relationships, and cast doubt on a company’s governance.

In this article, we’ll break down the key disclosure requirements by framework and region, explain when to begin preparations, and show what true ESG readiness looks like.

If you’re navigating individual ESG disclosures or sector-specific mandates, this guide will help ensure your enterprise is not caught unprepared.

Key reporting requirement deadlines by region and framework

When to begin prep upcoming ESG reporting deadlines

The safest rule for meeting ESG reporting deadlines for sustainability disclosures? Start 12–18 months before your first reporting period. That timeline gives you a full cycle to set boundaries, run a double materiality assessment, stand up data pipelines, and trial assurance.

If you’re newly in scope for CSRD compliance (large EU undertaking, listed SME, or non-EU parent) or operating under ISSB-aligned regimes, you’ll likely need the full 18 months the first time. U.S. state rules, such as California’s SB 253 and SB 261, demand similar lead time, particularly if this is the first time your organization will collect Scope 3 at scale or publish a TCFD-style risk report.

If your group reports across multiple jurisdictions, align on a single internal calendar with milestone gates every quarter. Centralizing your timeline reduces re-work and lets you rationalize external reporting windows so investor relations and assurance teams aren’t overwhelmed.

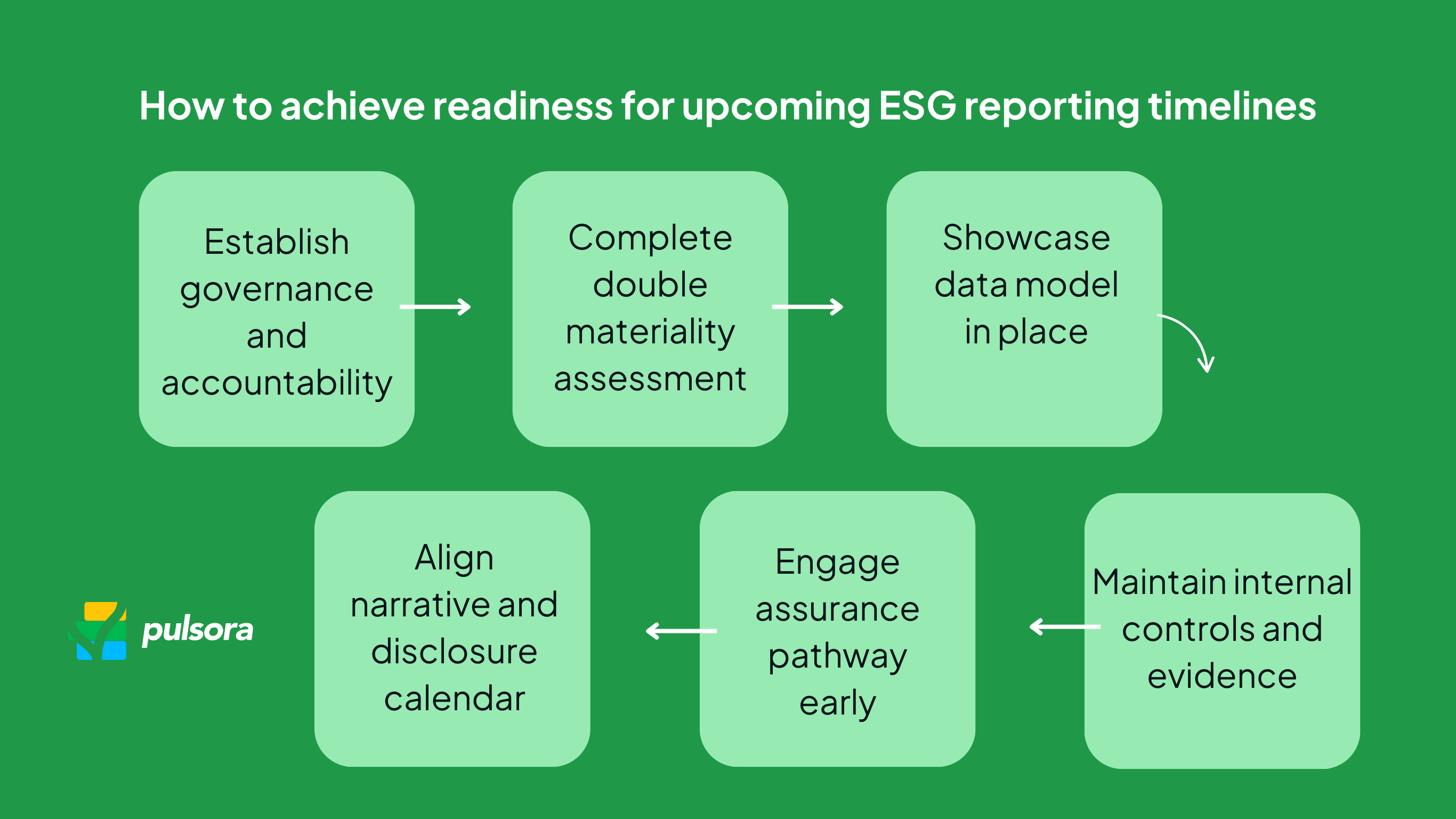

What readiness for reporting obligations looks like

Reporting readiness is what investors call “audit-ready.” You should be able to explain your scope, defend your methods, and reproduce your numbers. In practice, that means your program has seven elements in place before day one of the reporting period.

Governance and accountability

Your board charter or committee mandate covers sustainability oversight; management owns named topics with performance incentives aligned to targets.

Double materiality (or materiality) completed

You have a documented, repeatable assessment for ESG performance, and you can show why topics are in or out of scope. Next, you’ve mapped those topics to ESRS, ISSB, and GRI.

Data model and system of record

You streamline calculation methods across your supply chain (Scopes 1–3, water, waste, safety), define organizational and operational boundaries, and set up a central platform with audit trails and user permissions.

Internal controls and evidence

You can show source sustainability data, calculation steps, benchmarks, approvals, and change logs.

Assurance pathway

Your external assurance provider has scoped the engagement, flagged high-risk datapoints, and completed at least one “dry-run” review before year-end.

Narrative and KPIs

Your storyline matches your numbers. Strategy, risk, metrics, and targets connect clearly to what investors care about: resilience, capital allocation, and progress to goals.

Disclosure calendar and sign-offs

You’ve locked a calendar for each jurisdiction, aligned investor relations, legal, finance, and sustainability, and rehearsed approvals and XBRL/tagging where required.

Meet critical ESG reporting deadlines with Pulsora

As ESG reporting deadlines accelerate worldwide, enterprises need more than manual processes or spreadsheets.

Pulsora helps large organizations and SMEs centralize sustainability and carbon data, map disclosures to frameworks like CSRD, ESRS, ISSB, and state-level mandates, and ensure audit-ready accuracy. With automated workflows, built-in double materiality assessments, and assurance-ready outputs, Pulsora gives you confidence that your ESG reporting is complete, compliant, and aligned with investor expectations.

Ready to meet your next reporting deadline? Book a specialized demo to see how Pulsora can help your enterprise stay ahead.

FAQ

Q: When is the first CSRD report due for newly in-scope large EU undertakings?

A: Under the current deferral, the first reporting period is fiscal year 2027 with publication in 2028. Legacy NFRD entities reported for the financial year 2024 in 2025, and listed small and medium-sized enterprises begin with FY 2028 for publication in 2029.

Q: When should we start preparing ESG data for California SB 253?

A: Treat Scope 3 as an 18-month program in the first cycle of the reporting process. Most companies need supplier engagement, category prioritization, and assurance scoping cycles before data is investor-grade.

Q: Do we need assurance this year?

A: CSRD requires limited assurance already and moves toward reasonable assurance over time. Even where not mandated, limited assurance is increasingly expected by investors.

Q: Do EU companies have to report under CSRD right now?

A: Yes. The Corporate Sustainability Reporting Directive (CSRD) started phasing in from January 2024. Large EU public-interest companies (already subject to the NFRD) are the first wave, with their 2024 financial year reports due in 2025. From 2025 onward, large EU undertakings that meet two of three thresholds (250+ employees, €50M+ turnover, €25M+ assets) will also need to comply. Eventually, listed SMEs and even some non-EU companies with significant EU activity will be in scope.

Q: When do non-EU companies need to start reporting under CSRD?

A: Non-EU companies must also comply if they generate more than €150 million in annual EU turnover and have either a subsidiary or a branch generating significant EU revenue. These requirements apply starting with the 2028 financial year, with reports due in 2029.

Q: What are the key ESG reporting deadlines for non-EU companies outside of Europe?

A: Deadlines and initiatives vary:

- United States: While the SEC climate disclosure rule is no longer moving forward in its original form, state-level rules (such as California’s Climate Corporate Data Accountability Act) require certain disclosures starting in 2026.

- United Kingdom: Large companies must already disclose climate risks under the TCFD-aligned framework, with reporting continuing into 2025 and beyond.

- Japan, Singapore, Australia, and Canada: Each has climate- or sustainability-related disclosure rules either in place or moving toward alignment with ISSB standards (IFRS S1/S2) by the mid-2020s.

Q: What should enterprises outside the EU do to prepare for EU deadlines?

A: Even if headquartered outside Europe, if your business meets the €150M EU turnover threshold, you’ll need to start preparing now. This means:

- Mapping ESG data systems to CSRD/ESRS requirements.

- Running a double materiality assessment.

- Ensuring your disclosures are auditable and ready for assurance.