For sustainability professionals and private equity firms, understanding your carbon footprint has evolved far beyond measuring office electricity and business travel.

The real challenge and opportunity lies in accounting for financed emissions: the greenhouse gas impact of your loans, investments, portfolios, and other financial activities.

This is where the industry-led initiative for Partnership for Carbon Accounting Financials (PCAF) comes in.

What is PCAF?

PCAF is a global coalition of financial institutions working together to assess and disclose the greenhouse gas emissions (GHG emissions) and associated decarbonization efforts aligned with their loans and investments.

Founded in 2015 by 14 Dutch financial institutions, PCAF has rapidly expanded to become the industry standard for measuring financed emissions, with over 650 financial institutions now participating across five continents.

In 2018, PCAF expanded to North America and the Asia-Pacific market in 2021.

"As global interest grew, ABN AMRO, Amalgamated Bank, ASN Bank, Global Alliance for Banking on Values, and Triodos Bank decided to launch PCAF globally in 2019 with about 50 financial institutions. In 2023, PCAF became a non-profit entity with a Board of Directors,” their website reads.

At its core, PCAF provides the Global GHG Accounting and Reporting Standard for the Financial Industry — a comprehensive methodology that enables banks, investors, asset managers, and private equity firms to calculate and report the carbon footprint of their economic activities.

These three standards have been reviewed and approved by the Greenhouse Gas Protocol, or GHG Protocol, making them the recognized framework for Scope 3 Category 15 emissions in the financial sector.

Why PCAF matters for your organization

The numbers tell a compelling story.

For financial institutions, emissions tied to lending and investing activities account for over 99% of their total GHG inventory, with financed emissions averaging 750 times greater than direct operational emissions.

For private equity firms managing diverse portfolios, these financed emissions represent both significant climate impact and strategic opportunity.

In connection with the Paris Climate Agreement, which sets the universal goal of limiting global warming to well below 2°C/1.5°C, PCAF provides a map for sustainable finance to achieve that.

Beyond the environmental imperative, PCAF reporting offers tangible business benefits. It enables you to:

- assess climate-related risks in alignment with frameworks like the Task Force on Climate-related Financial Disclosures (TCFD)

- set science-based targets through the Science Based Targets initiative (SBTi)

- respond to investor demands for transparency

For PE firms seeking competitive advantages, PCAF-aligned reporting demonstrates sophisticated sustainability/ESG management and can differentiate your fund in an increasingly sustainability-conscious market.

Who needs to report?

While PCAF reporting remains voluntary for most institutions, regulatory and investor-driven disclosure frameworks — such as EDCI, CSRD, ISSB, and other emerging emissions data initiatives — depend on PCAF-aligned financed emissions calculations.

Financial institutions of all types can benefit from PCAF: banks, asset managers, pension funds, insurance underwriting companies, and private equity firms. The updated Standard covers diverse portfolios consisting of many types of financial instruments including loans, investments, and insurance products.

For private equity specifically, PCAF reporting helps general partners understand the carbon intensity of their portfolio companies and make more informed investment decisions. Even if you're not formally required to report today, regulatory momentum is building.

The EU's Corporate Sustainability Reporting Directive (CSRD), California's climate disclosure laws, and the International Sustainability Standards Board (ISSB) global baseline are all pushing financial institutions toward mandatory financed emissions disclosure. You can see overlapping data requirements below.

Early adopters gain a significant advantage: developing internal capacity now positions your organization ahead of regulatory requirements, investor expectations, and future-proofed decision-making.

Understanding the PCAF standard

The PCAF Standard covers three main areas, known as Parts A, B, and C:

Part A: Financed Emissions covers the emissions from your loans and investments across seven asset classes: listed equity and corporate bonds, business loans and unlisted equity, project finance, commercial real estate, mortgages, motor vehicle loans, and sovereign debt. This is the foundational piece that most organizations start with.

Part B: Facilitated Emissions addresses emissions from capital markets activities like underwriting and advisory services, where your institution facilitates rather than directly finances the transaction.

Part C: Insurance-Associated Emissions applies specifically to insurance companies, covering both underwriting activities and their investment portfolios.

The methodology requires calculating absolute emissions (measured in metric tonnes of CO2 equivalent or tCO2e) and attributing them proportionally to your institution based on your financing share. For example, if you hold 20% of a company's debt, you would account for 20% of that company's emissions.

PCAF’s core requirements and data needs

Implementing PCAF requires assembling several key data components:

Financial exposure data

Data gathered from your portfolio management systems, including outstanding loan amounts, equity positions, and asset values, is typically readily available from your existing financial systems.

Emissions data

Data gathered from your value chain, borrowers, and investees will ideally include their reported Scope 1 and Scope 2 emissions, and relevant Scope 3 emissions. This is where many organizations face their biggest challenge, as portfolio companies may not yet be measuring or disclosing their carbon footprints.

Asset-level information

Info such as company revenue, enterprise value including cash (EVIC), physical asset data like square footage for real estate or vehicle specifications for auto loans, and production metrics for certain sectors all fall under this requirement.

PCAF uses a data quality scoring system ranging from Score 1 (highest quality, using reported company emissions) to Score 5 (lowest quality, using economic-based estimations). Most organizations start with a mix of data quality scores and work toward improvement over time.

The key is to start measuring with the data you have available, even if it means initially relying more heavily on estimated emissions factors and industry averages.

Becoming a PCAF Signatory

PCAF operates as an industry-led collaborative where financial institutions become "signatories" by committing to measure and disclose their financed emissions. With over 650 signatories globally and 250+ having published disclosures, PCAF has grown from just 55 members at its 2019 global launch to become the financial sector's standard for GHG accounting.

The commitment

Signatories commit to assess and disclose GHG emissions from their loans and investments within three years using PCAF methodologies. Your first disclosure can focus on one asset class, a portfolio percentage, or specific funds—whatever fits your data availability. Climate goals focus on progressive improvement, not immediate perfection.

What you get

- PCAF Database: Exclusive access to emission factors updated twice yearly for filling data gaps

- PCAF Academy: Self-paced e-learning, case studies, and assessments for building internal capacity

- Technical Support: Webinars, one-on-one consultations, office hours, and documentation reviews

- Regional Networks: Implementation teams connecting you with peers facing similar challenges, particularly valuable for PE firms navigating LP reporting

- Working Groups: Direct input into Standard development and supplementary guidance

All of this is completely free—no membership fees, no methodology charges, no cost for technical assistance.

Why it matters

Signatory status signals proactive commitment to transparency and climate action. For private equity firms, it strengthens LP communications and differentiates your fund during fundraising. For all institutions, it positions you ahead of regulatory mandates and demonstrates alignment with investor ESG expectations.

Overlapping requirements: PCAF and other frameworks

As financial institutions face overlapping requirements from Corporate Sustainability Reporting Directive (CSRD) in the EU, California’s SB 253 and SB 261, ISSB’s IFRS S2, TCFD, Science-based Targets Initiative (SBTi), Carbon Disclosure Project (CDP), and the GHG Protocol, the challenge is no longer what to report—but how to do it efficiently and consistently.

The table below shows how PCAF functions as the common calculation backbone across these frameworks, enabling institutions to collect financed-emissions data once and reuse it across regulatory reporting, risk disclosures, target-setting, and investor questionnaires.

How to prepare for PCAF reporting

Starting your PCAF journey doesn't require perfection—it requires commitment and a systematic approach.

Step 1: Assess your portfolio composition

Identify which asset classes you hold and prioritize based on materiality. Many organizations start with listed equity and corporate bonds where emissions data is more readily available, then expand to private holdings.

Step 2: Evaluate your current data landscape

Inventory what financial and emissions data you already have access to through existing portfolio management systems, ESG questionnaires, and third-party data providers. Identify gaps and develop a data collection strategy, which may include engaging directly with portfolio companies, subscribing to emissions databases, or using estimation methodologies for hard-to-measure assets.

Step 3: Build internal capacity

Designate a cross-functional team spanning sustainability, risk, portfolio management, and data management. Consider joining PCAF as a signatory to access their academy training programs, database resources, and regional working groups where you can learn from peers navigating similar challenges.

Step 4: Start calculating

This is where PCAF meaningfully diverges from most other climate disclosures. Unlike high-level reporting frameworks, PCAF prescribes asset-class-specific calculation formulas, attribution rules, and data quality scoring requirements for financed emissions. Applying these consistently—especially at scale—is often the most technically demanding step of the process.

For each priority asset class, organizations must apply the relevant PCAF formula to calculate financed emissions, typically expressed as:

Financed emissions = Investee emissions × Attribution factor

Where the attribution factor varies by asset class (e.g., loans, private equity, listed equity, project finance) and depends on financial variables such as outstanding amount, enterprise value, or project ownership share. These methodological nuances matter: small differences in inputs or estimation approaches can materially change reported emissions and data quality scores.

A core challenge at this stage is data availability. Emissions data is often incomplete or unavailable for private investments, particularly in private equity and private credit portfolios. PCAF allows for multiple estimation pathways—ranging from reported emissions to sector-based or economic intensity proxies—but each pathway carries different implications for data quality scoring and audit defensibility. Choosing how to estimate is therefore not just a technical decision, but a reporting and governance one.

A second challenge is consistency at scale. Large financial institutions and private equity firms may be calculating financed emissions across hundreds or thousands of investments, each with different data maturity, ownership structures, and asset-class rules. Manually managing formulas, attribution logic, estimation hierarchies, and data quality scoring quickly becomes unworkable.

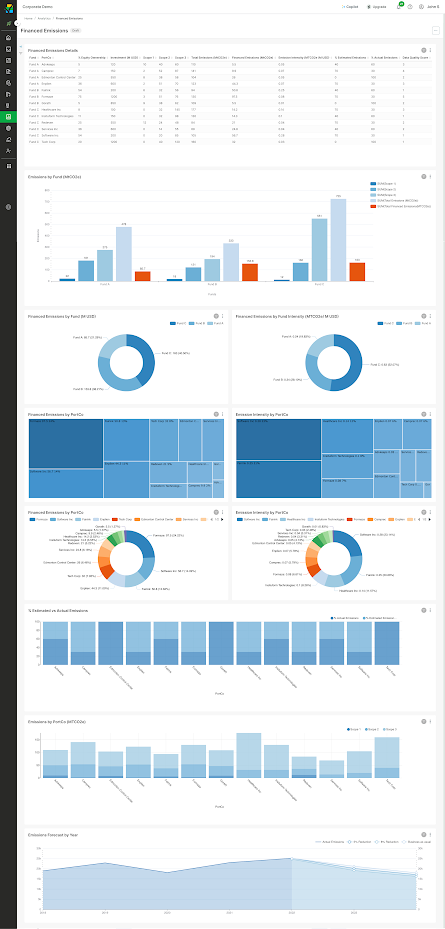

This is where purpose-built systems matter. Platforms like Pulsora operationalize PCAF by embedding asset-class-specific formulas, estimation hierarchies, and data quality scoring directly into the calculation workflow—allowing teams to apply PCAF consistently across large, complex portfolios.

The system preserves transparency by documenting data sources, assumptions, and calculation logic, while making it easier to identify data gaps and prioritize improvement over time:

Importantly, your first PCAF calculation is not expected to be perfect. Its real value lies in revealing where data is missing, where estimation choices materially affect results, and where portfolio engagement can improve future data quality. Treat this step as both a calculation exercise and a diagnostic—one that establishes a credible baseline and a clear roadmap for refinement in subsequent reporting cycles.

Step 5: Engage your portfolio

Reach out to portfolio companies that aren't yet measuring emissions and encourage them to begin. Many organizations find that their data collection process creates valuable dialogue with portfolio companies about climate strategy, often uncovering operational efficiency opportunities.

Step 6: Disclose and iterate

Report your findings, even if incomplete or heavily estimated. Transparency about data quality and improvement plans builds credibility. Commit to annual reporting with progressive data quality improvement.

The role of software in PCAF compliance

Given the complexity of data collection, calculation, and disclosure, software platforms have become essential enablers of PCAF reporting. Modern carbon accounting platforms designed for financial institutions can significantly streamline the process.

These platforms typically integrate with your existing portfolio management systems to automatically pull financial exposure data, reducing manual data entry and errors. They connect to multiple emissions databases and data providers, automatically matching your holdings with available company emissions data and filling gaps with appropriate emission factors when primary data isn't available.

Calculation engines built into these platforms apply the PCAF methodology consistently across asset classes, automatically calculating attribution factors based on your financing share and aggregating results to produce the absolute emissions and carbon intensity metrics required for disclosure. They track data quality scores according to the PCAF framework and often provide dashboards that help you visualize where data quality improvement efforts will have the greatest impact.

For general partners managing multiple funds, software solutions offer portfolio-level views while maintaining fund-specific reporting, support scenario analysis to model the impact of different investment decisions on portfolio carbon intensity, and generate audit trails and documentation necessary for third-party verification.

Perhaps most importantly, these platforms are continuously updated as standards evolve. PCAF recently launched updates to its Standard for Financed Emissions and Insurance-Associated Emissions, plus new supplemental guidance on Financed Avoided Emissions and Forward-Looking Metrics. Software providers incorporating these updates ensure your methodology remains current without requiring constant manual revisions to your calculation spreadsheets.

For private equity firms specifically, look for platforms that support deal-level analysis during due diligence, enable you to track emissions reduction progress across portfolio companies as part of value creation initiatives, and facilitate LP reporting with templates aligned to industry expectations.

PCAF: Implications and opportunities

The PCAF Standard represents more than a reporting obligation. It's a framework for understanding and managing climate risk while identifying opportunities in the transition to a low-carbon economy.

Over 650 financial institutions have joined PCAF to align their GHG assessment and disclosure with the accounting standards, creating a powerful network effect that's driving consistency and comparability across the industry.

For sustainability professionals, mastering PCAF is becoming as essential as understanding traditional financial metrics. For private equity firms, financed emissions reporting is evolving from a nice-to-have ESG initiative to a fundamental component of risk management and value creation.

The journey toward comprehensive financed emissions accounting takes time, but the destination—a portfolio strategy informed by robust climate data—offers both risk mitigation and competitive advantage.

The question is no longer whether to measure financed emissions, but how quickly you can build the capabilities to do so effectively.

With the right approach, adequate resources, and appropriate technology support, PCAF reporting transforms from a daunting compliance exercise into a strategic asset that strengthens your organization's resilience and reputation in a carbon-constrained future.

How Pulsora works with PCAF and financial products

PCAF sets a rigorous standard for financed emissions, but executing it at scale is where most teams struggle. Asset-class-specific formulas, multiple estimation pathways, data quality scoring, and thousands of investments quickly push spreadsheet-based approaches beyond their limits.

Pulsora operationalizes PCAF by embedding its methodologies directly into a single system of record. It applies PCAF formulas consistently, manages estimation logic and data quality transparently, and scales across complex portfolios—so the same financed emissions data can support PCAF disclosure, regulatory reporting, and investor requirements without rework.

For institutions treating PCAF as more than a one-time calculation, Pulsora turns compliance into a repeatable, decision-ready capability. Book a demo to learn more.