The final quarter of 2025 capped off a transformative year for ESG regulations and frameworks. Policymakers in major jurisdictions — from the European Union to the UAE — shifted focus from expansion to consolidation and simplification. Europe’s sweeping “Omnibus I” reforms marked a dramatic downsizing of sustainability reporting obligations, redefining the scope and scale of the CSRD and CSDDD. Meanwhile, in the U.S., the contrast between federal uncertainty and California’s state-level assertiveness deepened, as climate disclosure laws diverged in status and enforceability.

Asia-Pacific regulators, notably in Japan and Singapore, demonstrated strategic alignment with the ISSB’s global baseline, with Japan reaffirming its 2027 compliance roadmap and Singapore extending timelines for private firms. In the Middle East, the UAE took a forward-looking stance, unveiling comprehensive Climate Transition Planning Principles to operationalize decarbonization strategies.

Voluntary frameworks continued to evolve rapidly. The ISSB introduced targeted amendments to ease climate reporting burdens, GRI advanced its labor standards overhaul, and SBTi clarified its target review protocols. TNFD and SBTN made notable strides in scaling nature-related risk disclosures, including new data infrastructure plans and SME-focused tools. These developments signal a maturing ecosystem — one moving beyond policy ambition toward implementation precision.

Key regulatory and framework updates by region

Europe

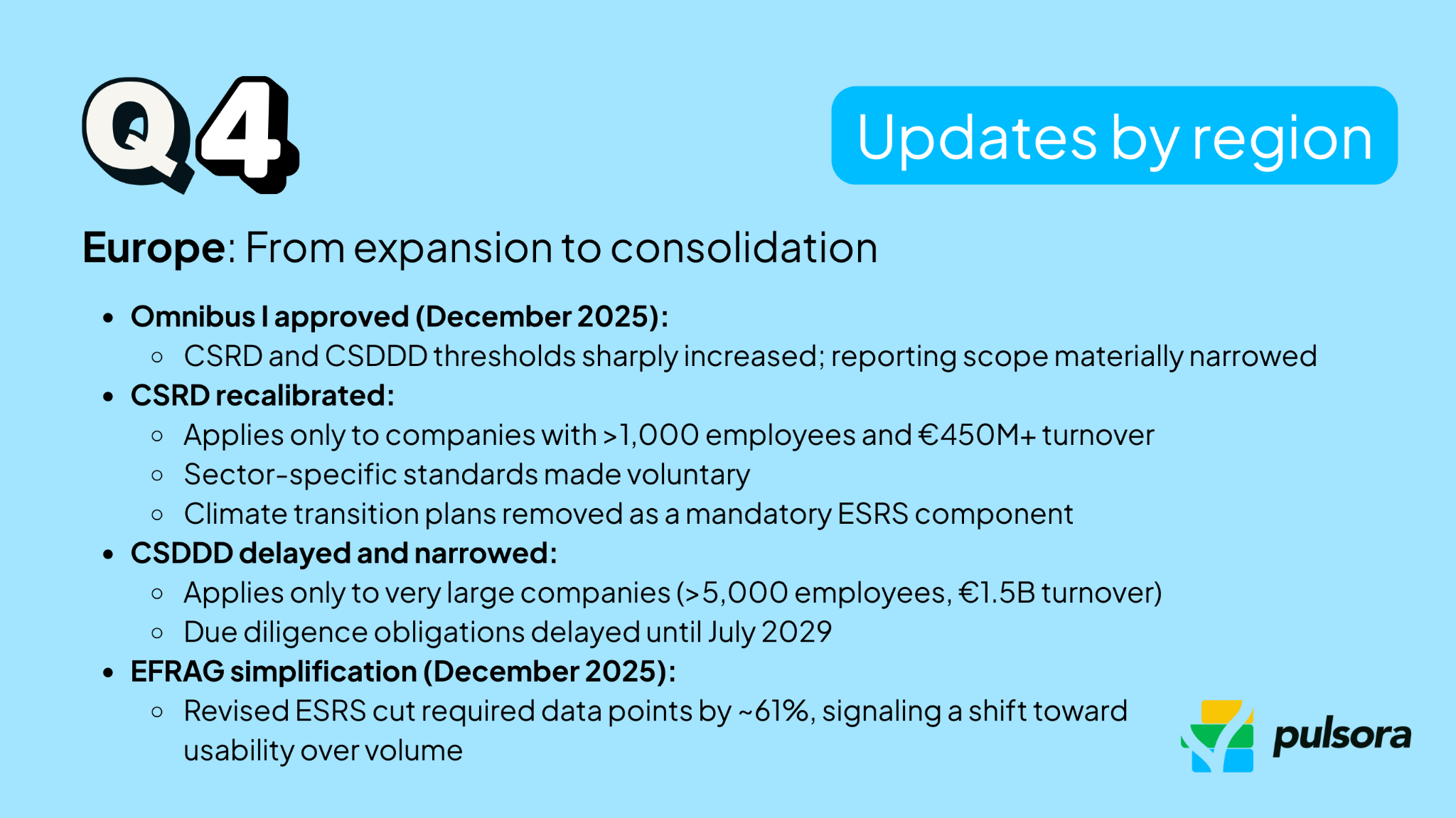

Simpler EU sustainability rules approved

On 16 December 2025, the European Parliament gave final approval to the “Omnibus I” reform package, dramatically scaling back EU sustainability reporting and due diligence requirements.

- The Corporate Sustainability Reporting Directive (CSRD) will now apply only to companies with

- >1,000 employees, a big jump from the previous >250 employee threshold

- > €450M+ turnover, a big jump from the previous >€50M+ turnover threshold.

- Sector-specific disclosures under CSRD are being made voluntary, and larger firms cannot pass down data demands to their small suppliers.

- Crucially, climate transition plans are no longer a mandated part of ESRS standards.

- Similarly, the Corporate Sustainability Due Diligence Directive (CSDDD) will now hit only the very largest companies (>5,000 employees, €1.5B turnover), and its human-rights and environmental due diligence duties won’t start until July 2029.

- The Council’s formal sign-off is expected imminently, and the new rules will enter into force 20 days after publication.

- In tandem, Europe’s accounting advisory body EFRAG delivered draft “simplified” reporting standards to implement the CSRD reforms: on 3 December, EFRAG submitted technical advice for revised European Sustainability Reporting Standards (ESRS), cutting required data points by 61% and greatly streamlining materiality assessments.

SFDR 2.0 proposal

In November, the European Commission turned its attention to the sustainable finance disclosure rules that apply to investors. On 20 November 2025 it unveiled a proposal to overhaul the Sustainable Finance Disclosure Regulation (SFDR). This “SFDR 2.0” aims to fix well-known shortcomings of the original regime – whose lengthy, complex fund disclosures often confused retail investors and were co-opted as de facto product labels. The Commission’s amendments would streamline what asset managers must report, make disclosures shorter and more usable for end-investors, and replace the rigid Article 6/8/9 product categories with a simpler classification. The SFDR overhaul is expected to be negotiated through 2026.

North America

US SEC climate disclosure

At the federal level, the much-debated SEC climate disclosure rule remained on hold through Q4 2025, as court challenges and political shifts left its status uncertain. The Securities and Exchange Commission did not attempt to enforce or implement its 2024 climate reporting rules amid ongoing litigation and a less supportive U.S. administration.

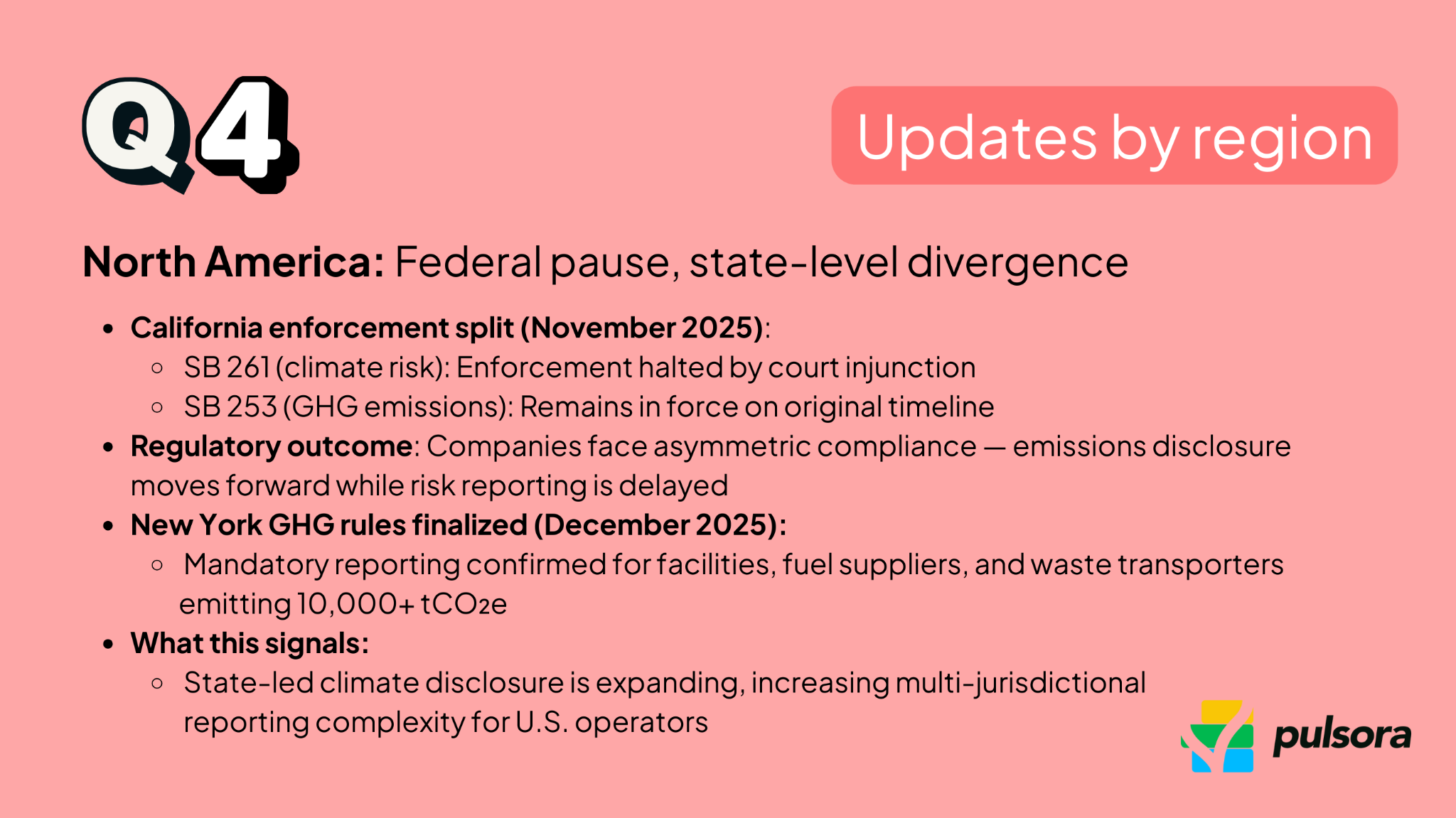

California’s climate laws

In contrast to federal inactivity, state-level climate disclosure took a dramatic turn in California this quarter. California had forged ahead with two new laws – SB 253 (mandating GHG emissions reporting) and SB 261 (mandating climate-related financial risk reporting) – but one of them hit a legal snag. On 18 November 2025, the U.S. Ninth Circuit Court of Appeals granted an injunction halting enforcement of SB 261 (the climate risk disclosure law) just weeks before companies’ first reports were due on 1 January 2026. Importantly, the injunction does not apply to SB 253, the law requiring disclosure of Scope 1, 2 (and eventually 3) emissions – that law remains in force on its original timeline. In response to the court order, the California Air Resources Board (CARB) announced it will not enforce SB 261’s January 2026 deadline and will set a new reporting date after the litigation is resolved.

New York confirms mandatory GHG reporting regime

In Q4 2025, New York finalized its long-awaited Mandatory Greenhouse Gas Reporting Program, establishing one of the most expansive state-level emissions registries in the U.S. The regulation requires facilities, fuel suppliers, and waste transporters emitting or supplying 10,000+ metric tons of CO₂e annually to begin collecting data in 2026, with first reports due June 1, 2027.

Notably, the rules apply even to companies headquartered outside New York if they supply fuel, electricity, or waste services into the state, reinforcing the growing reach of sub-national climate regulation amid federal uncertainty.

Asia-Pacific

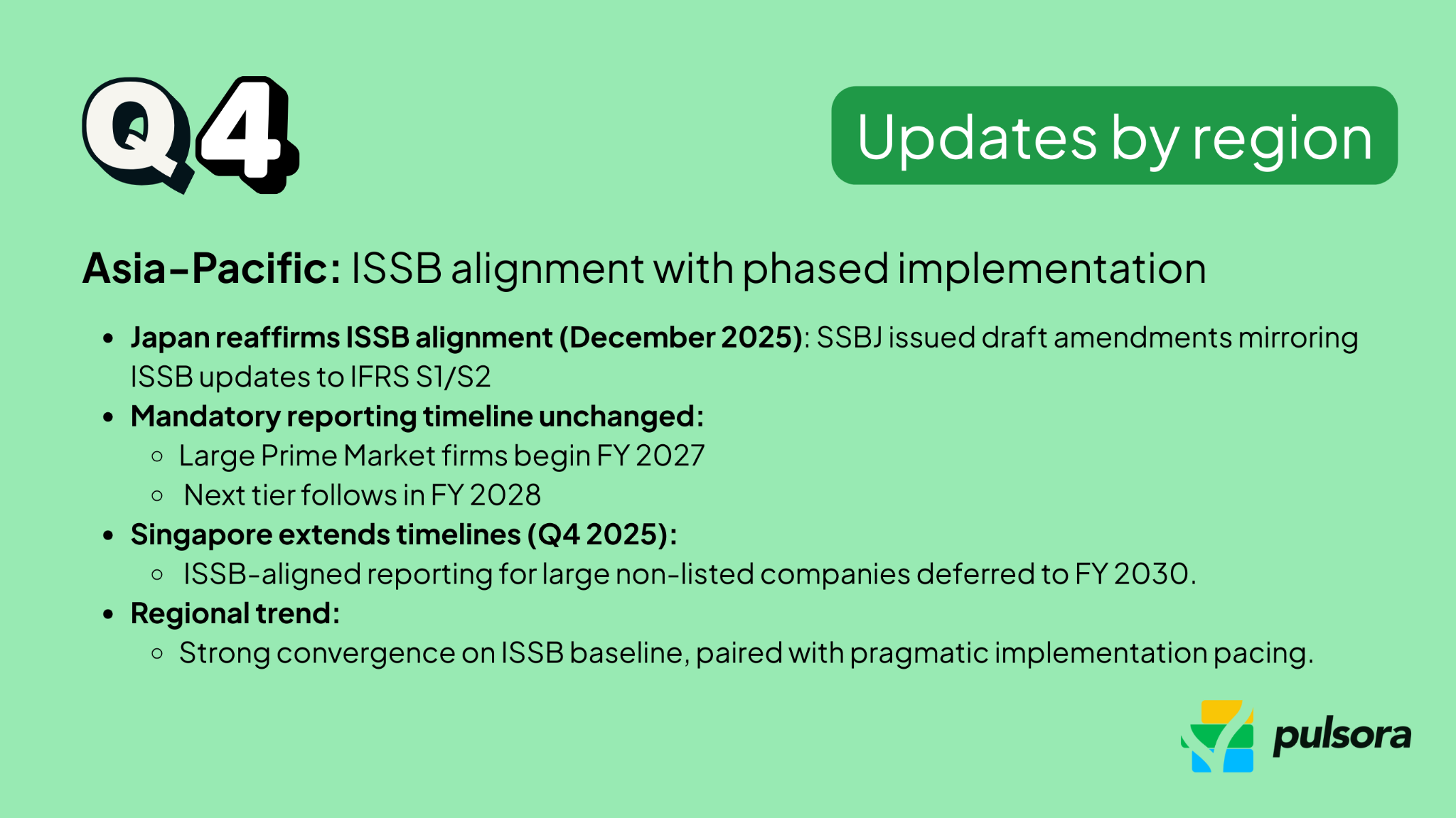

Japan aligns with ISSB’s updates

Japan reinforced its commitment to stay in lockstep with international standards. On 15 December 2025, the Sustainability Standards Board of Japan (SSBJ) issued a set of exposure drafts proposing amendments to Japan’s climate disclosure standards (J-IFRS S1/S2) to reflect the latest changes made by the ISSB. This was a direct response to the ISSB’s December update on greenhouse gas disclosures. By swiftly mirroring the ISSB’s tweaks, Japan is ensuring that companies using its standards won’t face conflicts with the global baseline. These amendments – covering technical points like financed emissions reporting – underscore that Japan’s forthcoming mandatory sustainability reporting (phased in from fiscal year 2027 for the largest firms) will remain “functionally aligned” with the ISSB Standards. In practice, Japan’s reporting roadmap stays on course: Prime Market companies above ¥3 trillion market cap are still expected to start reporting under SSBJ standards (equivalent to IFRS S1/S2) for FY 2027, with slightly smaller companies following in FY 2028.

Singapore extends timelines for private firms

Singapore made news by adjusting its climate reporting timetable to give companies, especially non-listed ones, more breathing room. The Accounting and Corporate Regulatory Authority (ACRA) and SGX Regulatory Co. announced extended deadlines for mandatory ISSB-aligned reporting by large unlisted companies. Under the revised roadmap, Scope 1 and 2 GHG disclosures and full ISSB-aligned climate reporting for big non-listed firms (>$1bn revenue) will now start in FY2030, instead of FY2027.

Other regions

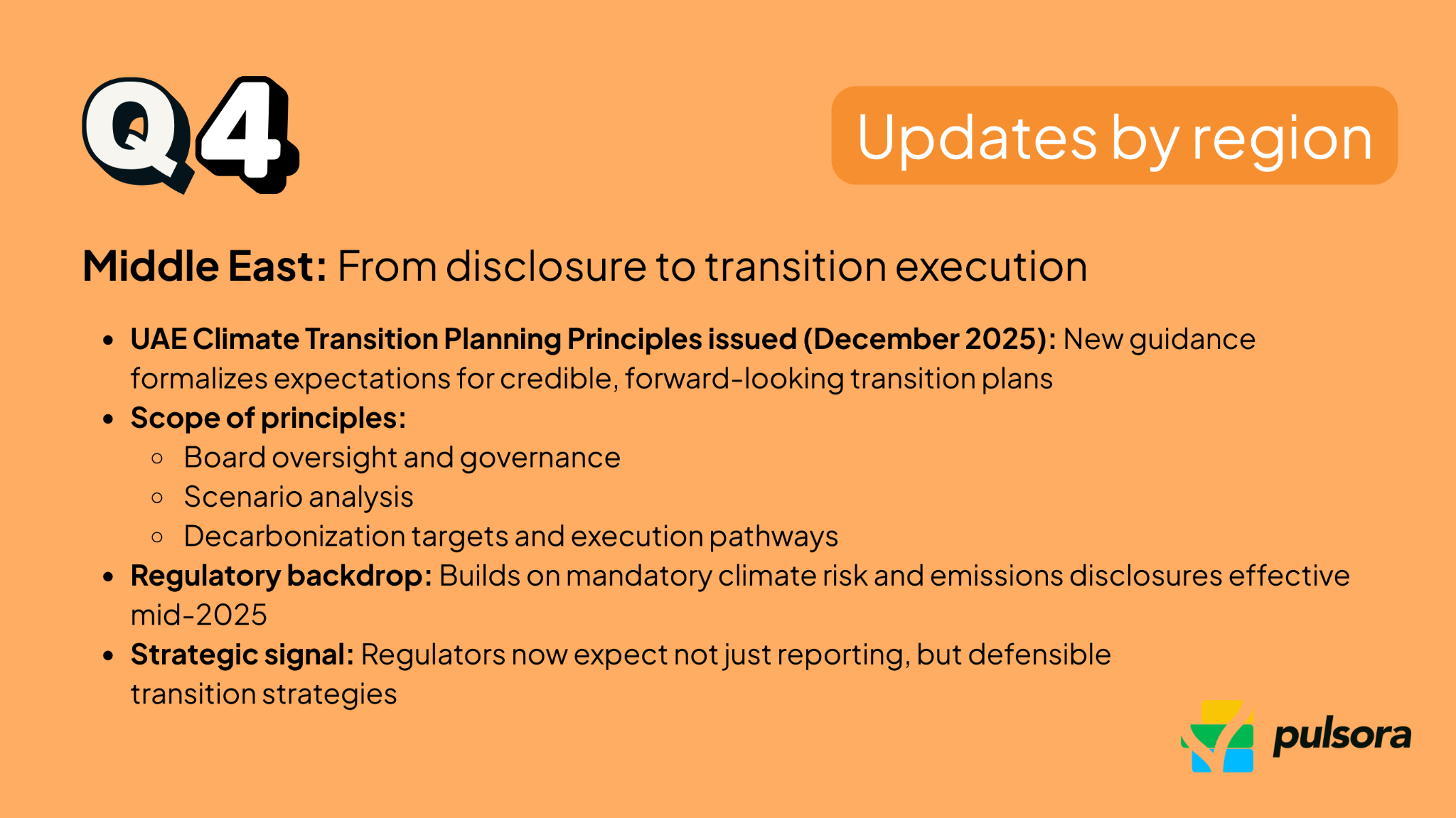

UAE advances its sustainable finance agenda

In the Middle East, the United Arab Emirates continued to lead with proactive sustainability policies. On 18 December 2025, the UAE Sustainable Finance Working Group – a coalition of UAE financial regulators and ministries – released its Fourth Statement summarizing progress on key ESG initiatives. A highlight of this Q4 update was the issuance of new “Climate Transition Planning Principles” for the UAE’s financial institutions and corporates.

These principles provide a unified framework for companies to develop and disclose credible climate transition plans, integrating aspects like board oversight, scenario analysis, and decarbonization targets into their overall governance. The Climate Transition Planning Principles complement earlier UAE initiatives – for instance, the mandatory climate risk and emissions disclosure requirements that took effect via the UAE Climate Change Law in mid-2025 (requiring large companies to report GHG emissions and climate risks). In essence, the UAE is creating a comprehensive ecosystem: taxonomy development, improved corporate governance on ESG, enhanced disclosure standards, and now detailed transition planning guidance.

For businesses in the UAE, Q4’s message was that regulators expect not just reporting of current impacts, but forward-looking plans for emissions cuts – with the Central Bank, securities regulators, and exchanges all backing this direction. Companies operating in the UAE should therefore beef up their internal climate strategies, as scrutiny on the plausibility of their transition pathways will rise.

Voluntary frameworks updates

Global Reporting Initiative (GRI)

Labor standards overhaul enters final phase: The GRI pushed forward with its comprehensive update of labor-related reporting standards in Q4. On 10 December 2025 (International Human Rights Day), GRI launched a public consultation on draft revisions to four key GRI Topic Standards covering workers’ rights. The standards under review address

- Workers in Business Relationships (GRI 414)

- Forced Labor (GRI 409)

- Child Labor (GRI 408)

- Freedom of Association and Collective Bargaining (GRI 407)

The consultation runs until March 2026, after which GRI’s Global Sustainability Standards Board will finalize the standards (expected to be issued in late 2026). Once in effect, these updated GRI standards will raise the bar for social sustainability reporting. Companies using GRI (which is still the world’s most widely used ESG reporting framework) will need to gather more granular information on labor rights performance.

International Sustainability Standards Board (ISSB)

The ISSB issued its first revisions to the IFRS Sustainability Disclosure Standards in Q4, focusing on clarifying and easing certain climate-related requirements. On 11 December 2025, the ISSB published “Amendments to Greenhouse Gas Emissions Disclosures”, an update to IFRS S2 Climate-related Disclosures. This amendment package includes:

- Relief for financial institutions on Scope 3 Category 15 (investment portfolio) emissions – allowing banks and asset managers to limit disclosure to their financed emissions and omit other portfolio emissions like derivatives. Firms using this relief must explain any exclusions and still report their total financed emissions.

- Additionally, the amendments permit use of alternative GHG accounting approaches if required by local regulators (e.g. different global warming potential values), aiding jurisdictional alignment. These changes will take effect for annual reporting periods beginning January 1, 2027, with early adoption allowed.

- ISSB also concurrently updated the SASB Standards (industry-specific metrics) to align with these changes – part of its effort to maintain the “global baseline” as a living, responsive framework.

With this done, the ISSB signaled that its next focus may turn to new topic areas in 2026 (such as biodiversity or human capital), now that the climate standard is in application mode.

Science-Based Targets Initiative (SBTi)

In November 2025, SBTi released a second consultation draft of Net-Zero Standard Version 2.0. This forthcoming standard (expected 2026) will likely raise the ambition level and clarify long-term net-zero criteria.

Additionally, On 11 December 2025, SBTi released a set of resources detailing how to conduct these “mandatory five-year target reviews” and how SBTi will reflect target status changes publicly. This included a Five-Year Target Review Guidance document and manual, which walk companies through evaluating whether their existing targets (set ~5 years ago) still meet current SBTi criteria, and if not, how to update them. Alongside this, SBTi introduced expanded “commitment and target status” categories on its public dashboard. As companies go through the review cycle, their status may be labeled as “Active – Under Review” or “Updated” or “Expired” etc., improving transparency for stakeholders looking at the SBTi Target Dashboard. For example, early adopters who set targets back in 2018/2019 are now reaching the five-year mark – they will need to reaffirm or adjust their targets in 2024–2025. SBTi’s new guidance makes this process more straightforward and signals to the market which companies are keeping their climate commitments current.

SBTN (The Science Based Targets Network)

The SBTN – which develops methods for companies to set targets on nature (water, land, biodiversity, oceans) – made significant progress in Q4 2025 as it transitions from pilot phase toward broader adoption.

On 30 October 2025, the Science Based Targets Network launched the Step Up for Nature initiative so companies can collectively signal their ambition for credible nature action. This initiative invites companies to signal their intent to set approved targets for freshwater, land, oceans, and biodiversity, even before all methodologies are fully available.

According to SBTN’s end-of-year report (released 17 December 2025), over 150 companies are now actively engaging with SBTN’s framework, preparing to set science-based targets for nature. In fact, 25 companies publicly announced new commitments or “stepping stone” milestones toward nature targets in 2025. Big names like Holcim (building materials) and GSK (pharma) were among those sharing progress, with Holcim setting new water targets and GSK setting its first land targets for ecosystem impacts.

TNFD (Taskforce on Nature-related Financial Disclosures)

On October 2, 2025, TNFD released a set of eight recommendations for upgrading the nature data value chain for market participants, including a blueprint to govern, launch, operate and finance a Nature Data Public Facility (NDPF) first proposed by the TNFD in 2023. This is a step toward integrating nature-related risks into mainstream financial analysis, enabling more robust corporate disclosures aligned with the TNFD framework.

On November 14, 2025, TNFD launched an Innovation Challenge focused on democratizing nature intelligence for SMEs and local actors. In collaboration with the UN Environment Programme World Conservation Monitoring Centre (UNEP-WCMC), this initiative invites innovators to develop tools that enable smaller enterprises to assess and report on nature-related risks. This signals TNFD’s intent to scale adoption beyond large corporates, aligning biodiversity risk assessment across the value chain.

Additionally, the ISSB announced its decision to explore future standard-setting work on nature, indicating that it will draw from the TNFD framework as a foundational reference. This recognition positions TNFD as the baseline framework for future global nature-related disclosure standards, paving the way for formal integration with ISSB’s sustainability reporting architecture.

Impact on companies & investors

The Q4 2025 changes carry meaningful implications for sustainability teams, compliance leads, and investors:

- Scope and complexity reduction: Companies previously caught in the crosshairs of emerging ESG mandates—especially in the EU—will find relief in narrowed applicability thresholds and simplified reporting requirements.

- Preparation still required: Despite simplifications, large corporates and financial institutions must remain vigilant. Streamlined doesn’t mean optional—especially as regulators sharpen expectations around data quality, transition plans, and downstream impacts.

- Jurisdictional fragmentation: The divergence between federal and subnational policies in the U.S., along with differing regional timelines in Asia, means multinational companies will need region-specific ESG strategies to remain compliant.

- Investor focus on credibility: With frameworks like SBTi and TNFD tightening guidance and increasing transparency, ESG-labeled funds and corporates will face greater scrutiny over the credibility and integrity of their claims.

- Nature rising: The integration of TNFD with ISSB planning, and growing momentum around nature targets from SBTN, point to 2026 being a breakout year for nature-related disclosures—no longer optional for ESG leaders.

Looking ahead to 2026

As we enter 2026, several themes are set to define the ESG landscape:

- Standardization and convergence: Expect accelerated work from ISSB, EFRAG, and other standard setters to align climate and nature reporting frameworks into a unified global architecture, reducing fragmentation while raising expectations.

- Nature-related reporting frontiers: Biodiversity, freshwater, and land-use impacts will dominate disclosure pilots and early adopter strategies, as TNFD and SBTN prepare for broader implementation.

- Enforcement and litigation: Legal challenges to ESG laws—particularly in the U.S.—will continue shaping how rules are enforced. Yet regulatory momentum is unlikely to stall, especially at the state and global levels.

- Data quality and tech integration: With new nature and labor standards on the horizon, the focus will shift from reporting volume to data credibility. Companies will need better systems, assurance mechanisms, and cross-functional ESG expertise.

In short, Q4 2025 marked a pivot from ESG expansion to ESG execution. As 2026 unfolds, companies that embed agility, transparency, and accountability into their ESG programs will be best positioned to thrive.