EU policymakers introduced a formal Stop-the-Clock delay and reached a provisional agreement on a broader Omnibus simplification package, reshaping who is in scope, when reporting begins, and how companies should prioritize readiness.

These changes narrow applicability and extend timelines for many organizations — but they do not remove the underlying expectation that sustainability data be accurate, defensible, and decision-useful.

As a result, CSRD readiness today is less about reacting to a single reporting deadline and more about building durable reporting foundations: governance, materiality, data systems, internal controls, and assurance pathways that can withstand regulatory scrutiny as requirements finalize.

Whether your organization is required to report in the near term, later this decade, or is reassessing applicability under the latest EU developments, a structured approach to CSRD readiness remains critical. Companies both in the EU and across the globe that treat this period as preparation time — rather than a pause — will be best positioned to respond as final rules are adopted and expectations continue to rise.

The following ten steps outline what CSRD readiness looks like in practice and how companies can move forward with clarity amid regulatory change.

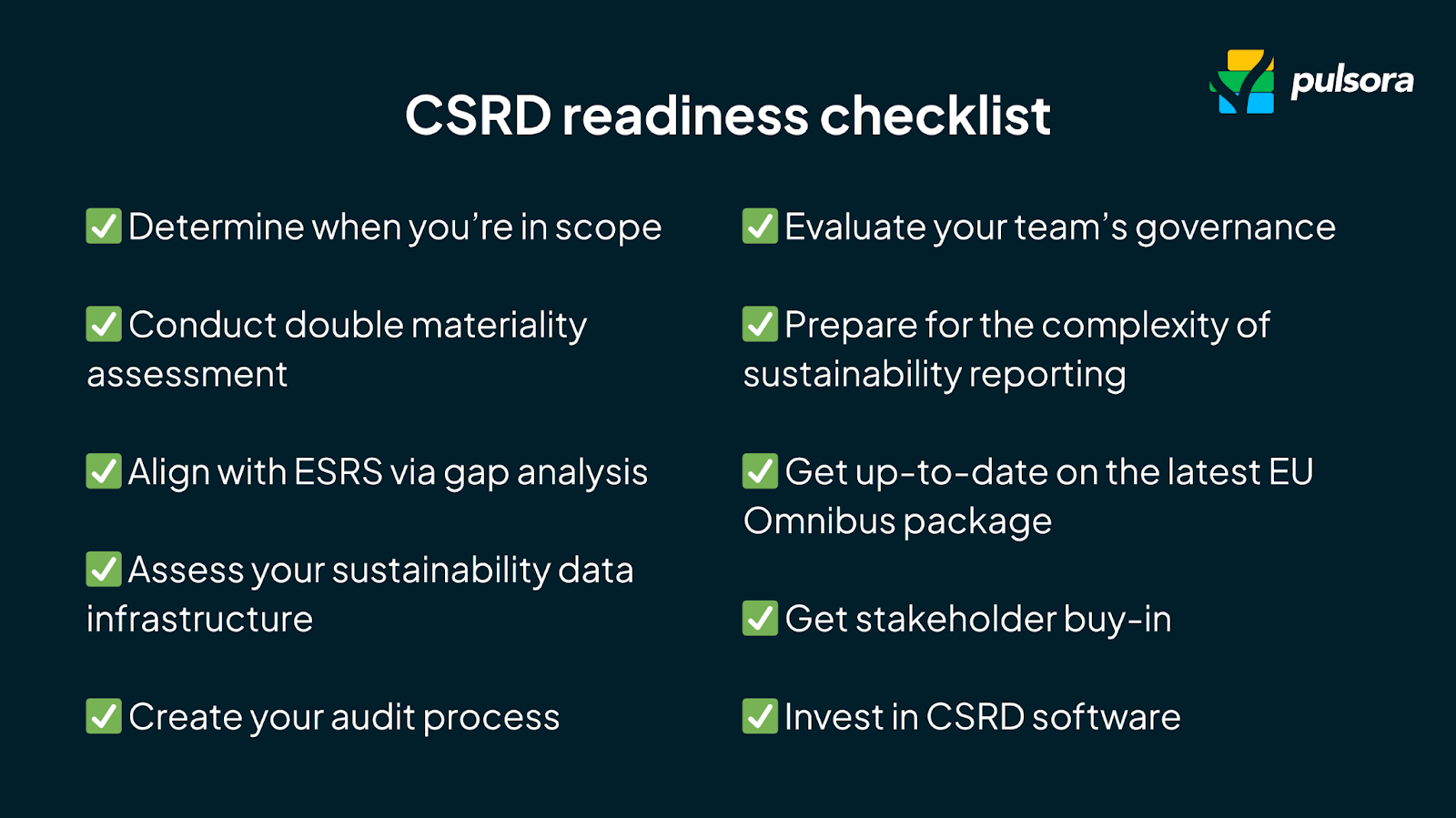

Checklist to determine CSRD readiness and reporting scope

10 ways to ensure CSRD readiness and compliance

1. Determine whether (and when) you're in scope

Who does the CSRD apply to (as of Dec 30, 2025)? The Corporate Sustainability Reporting Directive applies to the largest companies with significant economic footprints. Following the provisional agreement on the EU’s Omnibus simplification package (approved by the European Parliament on Dec 16, 2025), CSRD will apply to companies that meet both of the following criteria once the final text is published and enters into force:

More than 1,000 employees, and

Annual net turnover of more than €450 million within the EU. These revised thresholds substantially narrow the number of companies in scope compared with earlier drafts. Non-EU parent companies with a substantial EU turnover are also impacted (via Consilium).

Action if not ready:

Conduct a scoping review based on workforce size, revenue, and location.

Monitor updates from EFRAG and the EU Commission.

Pay attention to exemptions for listed SMEs and consolidated reporting.

2. Complete a double materiality assessment

Why it matters: Under CSRD, companies must assess both how sustainability issues impact their financial performance (financial materiality) and how they impact people and the planet (impact materiality).

What readiness looks like: You've conducted a documented and stakeholder-informed assessment, with clear prioritization of ESG topics across your value chain.

Action if not ready:

Engage stakeholders, including investors, suppliers, and affected communities.

Use software tools or consultants to document and justify your approach.

Revisit your DMA annually for evolving risk management protocol.

💡 Considering solutions for managing end-to-end CSRD compliance? Check out our CSRD buying guide to choose the right tool for you.

3. Conduct a gap analysis against ESRS

Why it matters: The ESRS includes dozens of disclosure requirements across environmental, social, and governance topics. Most companies aren’t starting from scratch — but few are fully aligned either.

What readiness looks like: You’ve mapped your existing ESG reporting to CSRD’s reporting obligations and identified where disclosures fall short, especially for data points like biodiversity, water usage, or social metrics.

Action if not ready:

Download the ESRS templates and crosswalk them with your current reports.

Prioritize high-impact gaps aligned with your materiality assessment using data management software.

Create a phased roadmap to close the gaps ahead of your first reporting year.

4. Assess your sustainability data infrastructure

Why it matters: CSRD isn’t just about what you disclose; it’s about how you gather and validate your sustainability data. This includes emissions, workforce metrics, and other ESG indicators, often spread across multiple departments and systems.

What readiness looks like: Your data collection process is automated, structured, and centralized—with audit trails and traceability in place.

Action if not ready:

Inventory your ESG data sources and tools.

Invest in platforms that support CSRD reporting, data validation, and integration with ERP systems across your supply chain.

Focus on high-risk areas like Scope 3 emissions, biodiversity, and workforce data.

5. Define your audit and assurance process

Why it matters: Under CSRD, sustainability disclosures must be independently assured. Limited assurance is required now, but companies must prepare for reasonable assurance in the future.

What readiness looks like: You’ve already looped in internal audit and external assurance providers, built version control and documentation workflows, and can clearly trace every disclosed figure.

Action if not ready:

Define internal roles and responsibilities for assurance.

Build or optimize workflows for evidence tracking and version management.

Monitor the European Commission’s evolving guidelines on assurance practices.

6. Evaluate your governance and internal accountability

Why it matters: CSRD requires companies to disclose how sustainability is governed: who’s responsible, how it’s embedded in strategy, and what oversight exists.

What readiness looks like: You have an ESG or sustainability committee at the board level, and executive accountability for sustainability topics.

Action if not ready:

Define sustainability oversight roles for your C-suite and board.

Include CSRD metrics in executive performance goals.

Document your governance structure in line with ESRS G1 requirements.

7. Prepare for reporting process complexity

Why it matters: CSRD reporting is not a one-time PDF. You’ll need to publish a digital, machine-readable sustainability statement alongside your annual report. And, if you’re a multinational group, you may need to consolidate multiple sustainability statements.

What readiness looks like: You’ve already designed your reporting process and workflows, including XBRL formatting, legal review, and sustainability data signoff.

Action if not ready:

Outline a reporting calendar with clear internal deadlines.

Select a reporting platform that supports ESRS templates and tagging.

Coordinate with legal, finance, and IT to streamline the reporting process.

8. Understand the implications of the Omnibus simplification package

Why it matters: The EU’s policy developments in 2025 — including the Stop-the-Clock Directive and the Dec 2025 Omnibus simplification agreement (provisionally approved by Parliament on Dec 16, 2025) — do more than just offer short-term deferrals. Together, they:

Legally defer reporting deadlines for many companies until later waves (e.g., Wave Two reporting in 2028 and non-EU parent reporting in 2029)

Raise scope thresholds (e.g., >1,000 employees and >€450 million turnover) that will apply once final law is published

Introduce more proportional and risk-based requirements while preserving ESRS-aligned reporting and double materiality

Companies should interpret these developments as a recalibration of timing and applicability, not as broad exemptions, and continue preparing foundational governance, data, and assurance infrastructure.

9. Align teams and educate stakeholders

Why it matters: CSRD touches nearly every department: finance, operations, HR, procurement, legal, investor relations, and more.

What readiness looks like: You’ve formed a cross-functional CSRD task force with clear ownership, regular check-ins, and defined deliverables.

Action if not ready:

Conduct CSRD readiness workshops with internal teams.

Identify training needs, especially around materiality, assurance, and data governance.

Bring in external consultants or auditors as needed to accelerate internal understanding.

10. Invest in CSRD-ready reporting software

Why it matters: Manual reporting is time-consuming, error-prone, and difficult to audit. A purpose-built platform can streamline everything from data collection to final report generation.

What readiness looks like: You’ve implemented a tool that supports sustainability disclosures, integrates with your existing systems, and helps you manage regulatory updates.

Action if not ready:

Evaluate CSRD software platforms based on features like audit trails, ESRS mapping, and scalability.

Select a solution that supports not just compliance, but better ESG decision-making across your company.

Look for platforms that provide built-in templates, workflow automation, and assurance readiness.

Your journey to CSRD preparedness starts today

CSRD compliance isn’t a finish line; it’s a long-term transformation of how your company operates, measures, and communicates sustainability performance.

By focusing on these 10 steps, you can turn compliance into opportunity, build trust with your stakeholders, and lead the market in transparency.

How Pulsora helps companies operationalize CSRD readiness

Pulsora’s sustainability management platform is purpose-built to support every step of your CSRD readiness journey. from ESG data integration to audit-ready reporting aligned with the European Sustainability Reporting Standards (ESRS).

Whether you're navigating Wave One disclosures or building a roadmap for future compliance, Pulsora helps you streamline the reporting process, eliminate data silos, and ensure you're always prepared for evolving CSRD requirements.

Frequently Asked Questions about ways to prepare for CSRD

What is CSRD readiness?

CSRD readiness refers to how prepared a company is to meet the reporting and disclosure requirements under the Corporate Sustainability Reporting Directive (CSRD). This includes understanding whether your company is in scope, conducting a double materiality assessment, ensuring data quality, building audit readiness, and aligning with the European Sustainability Reporting Standards (ESRS).

Who does the CSRD apply to?

Under the provisional EU Omnibus simplification agreement (Parliament approved Dec 16, 2025) and the Stop-the-Clock Directive, the directive will apply to companies that meet both of the following once the text is finally adopted and published:

Large companies with >1,000 employees and >€450 million net turnover

Non-EU companies with ≥ €450 million EU turnover and an EU subsidiary/branch of sufficient size

Thresholds for listed SMEs and other categories have been narrowed or removed under the negotiated outcome, significantly reducing the total number of companies in scope compared with earlier drafts.

How can I tell if my company needs to report under CSRD?

To determine if your company needs to report, conduct a scoping assessment against the latest EU thresholds. As of late 2025, the directive — when finalized — will generally capture companies with >1,000 employees and >€450 M in net EU turnover. The Stop-the-Clock Directive has legally shifted many reporting timelines (e.g., Wave Two companies reporting FY 2027 data due 2028), and the Omnibus simplifications narrow the in-scope population.

What is a double materiality assessment?

A double materiality assessment is a core CSRD requirement that evaluates:

Financial materiality – how sustainability issues affect your business

Impact materiality – how your business impacts people and the environment

This assessment determines which topics your company is required to report on under the ESRS and must be well-documented and stakeholder-informed.

What are the ESRS and why do they matter?

The European Sustainability Reporting Standards (ESRS) are the mandatory disclosure framework for CSRD. They define what companies must report across environmental, social, and governance categories and provide the structure for your sustainability statements. CSRD readiness requires alignment with these standards.

What data do I need to report under CSRD?

You must report structured, verifiable data on ESG performance—including greenhouse gas emissions (Scopes 1, 2, and 3), energy use, workforce metrics, governance practices, and more. CSRD also requires forward-looking information, such as sustainability targets and transition plans.

What is the difference between limited assurance and reasonable assurance?

Under CSRD, companies must obtain third-party assurance of their sustainability disclosures.

Limited assurance is a preliminary review to verify plausibility.

Reasonable assurance is more rigorous and comparable to a financial audit.

CSRD will phase in a transition from limited to reasonable assurance over time.

How can software help with CSRD compliance?

CSRD-ready software can automate data collection, facilitate double materiality assessments, align your reports with the ESRS, and build in audit-ready documentation. It’s especially critical for large companies or non-EU multinationals managing data across multiple entities and geographies.

How has the EU Omnibus “quick fix” changed CSRD requirements?

The EU Omnibus simplification package, provisionally agreed in December 2025 and approved by the European Parliament, reshapes CSRD by:

Deferring reporting dates for many companies under the Stop-the-Clock Directive

Substantially raising scope thresholds (e.g., >1,000 employees, >€450 M turnover)

Simplifying some reporting burdens while preserving core requirements such as ESRS-aligned disclosures and double materiality

These changes are expected to be formally adopted and published in early 2026.

What happens if I don’t comply with the CSRD?

Failure to comply with CSRD can result in regulatory penalties, reputational damage, and loss of investor trust. Because CSRD disclosures are intended to be public and auditable, inaccuracies or omissions can also create legal and operational risk. Preparing early is key to avoiding last-minute scrambling and ensuring your disclosures are accurate and meaningful.