Q2 2026 was defined by execution and recalibration rather than expansion. The first mandatory reporting seasons arrived. Australia’s first sustainability reports landed, and the United States spent the quarter recalibrating its own timelines. Regulators across major markets pressed ahead with simplification, trimming data requirements while holding the line on core disclosure.

The clearest divergence was again transatlantic. The U.S. SEC moved to formally rescind its 2024 climate-disclosure rules, and Brazil shifted its ISSB-based regime from mandatory to voluntary. The EU advanced, rather than abandoned, its simplified ESRS, and both the EU and UK consulted on lighter-touch, investor-facing rules.

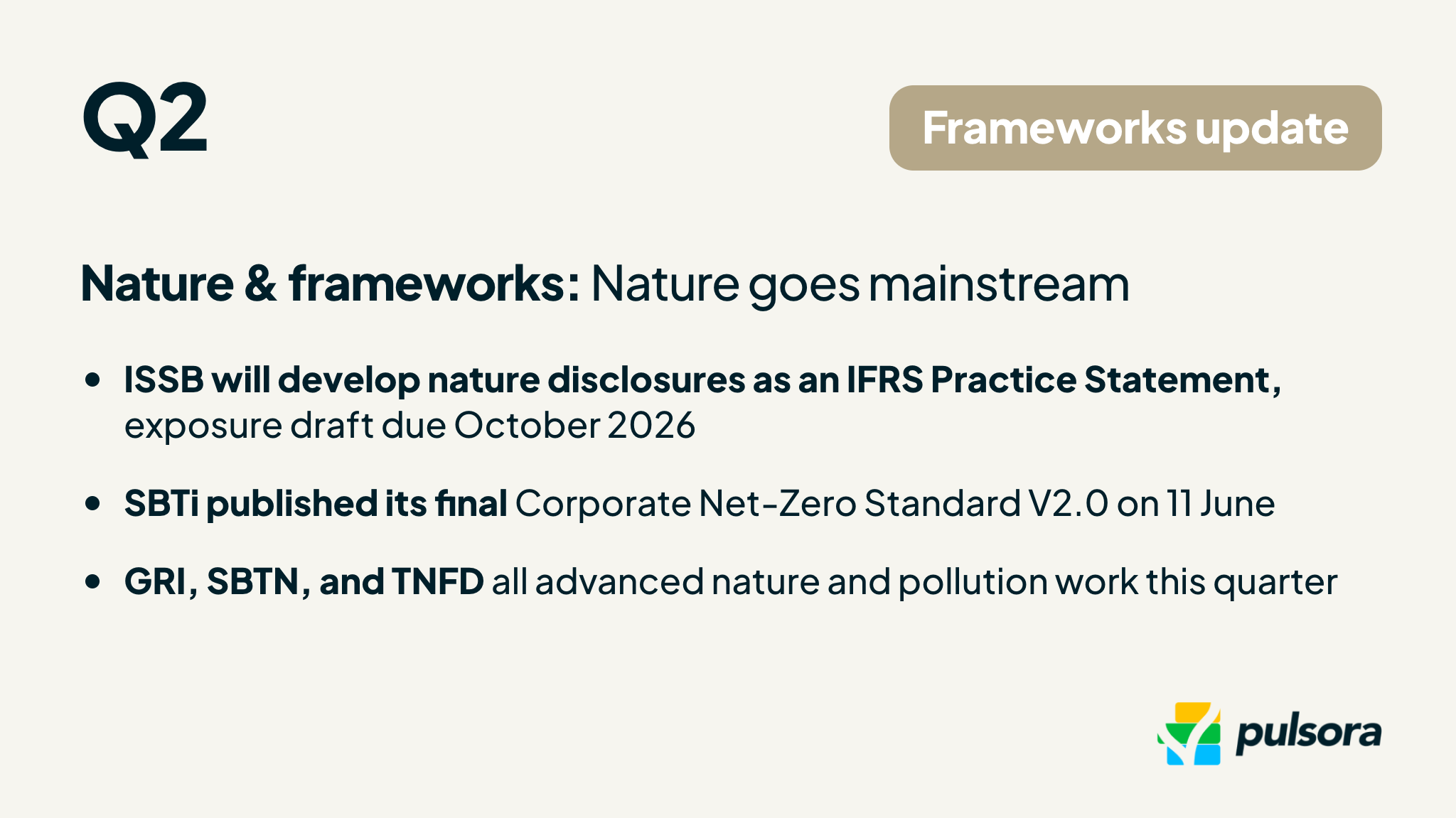

Nature moved from promise to plan. The ISSB agreed the form of its nature-related disclosures, SBTi finalized its Corporate Net-Zero Standard V2.0, GRI consulted on pollution standards, and TNFD and SBTN advanced practical tooling. Together they confirmed that biodiversity and broader nature impacts are entering the disclosure mainstream.

For financial markets, the quarter reinforced a two-speed reality. Headline mandates are being pared back in some jurisdictions, but investor-facing standard setters keep raising the bar on comparability, assurance, and nature.

Takeaways for business & finance

- Simplification is now the dominant regulatory mode: From the EU’s revised ESRS to EBA supervisory reporting and UK product disclosures, the Q2 direction was burden reduction, with core reporting left intact.

- Divergence is widening, not closing: The U.S. (SEC rescission proposal) and Brazil (mandatory to voluntary) stepped back, even as Australia and Japan operationalized mandatory ISSB-aligned regimes.

- The first reporting seasons are here: Australia’s regulator published early observations on the first lodged reports, and California’s first SB 253 deadline moved rather than vanished. Execution, not policy, is the near-term test.

- Nature is now a standard-setting workstream: ISSB confirmed an IFRS Practice Statement approach for nature, SBTi’s Net-Zero V2.0 landed, and GRI, SBTN, and TNFD all advanced.

- Assurance is the next frontier: Japan confirmed mandatory limited assurance and Australia engaged audit firms on methodologies. Data credibility, not just disclosure, is the rising bar.

Key regulatory and framework updates by region

Europe

The EU continued implementing its “Omnibus” simplification. On 6 May 2026, the European Commission published a draft delegated act containing the revised, simplified first set of ESRS, cutting mandatory data points by more than 60%, alongside a draft voluntary standard for smaller companies. The Commission opened a one-month feedback period, which closed on 3 June 2026. The act was not yet formally adopted, with the revised standards expected to apply for financial years beginning on or after 1 January 2027. This follows the Omnibus reforms that reshaped CSRD and CSDDD scope earlier in the year.

On 29 April 2026, ESMA opened a consultation on endorsement guidelines for non-EU ESG ratings under the ESG Rating Regulation, ahead of the regime’s 2 August 2026 application date. The “SFDR 2.0” review advanced to committee stage in the European Parliament, the EBA opened a consultation to simplify supervisory reporting with a dedicated ESG module on 10 April 2026, and the Commission’s revision of EU Taxonomy screening criteria closed for feedback on 14 April 2026.

North America

USA

Federal climate disclosure moved decisively in reverse. On 29 May 2026 the SEC voted to propose rescinding its 2024 climate-disclosure rules in full. The proposed rule was published on 3 June 2026 and is open for comment through 3 August 2026. The 2024 rules had never taken effect amid litigation.

California remained the counterweight. Following its March workshop, CARB ran a pre-rulemaking comment period that closed 13 April 2026 on concepts for full Scope 1, 2, and 3 reporting from 2027. Late in the quarter, on 24 June 2026, CARB announced it intends to defer the first SB 253 Scope 1 and 2 reporting deadline from 10 August 2026 to 10 November 2026, with no template or assurance required for first-year reports. SB 261 remained enjoined pending the Ninth Circuit appeal. The deadline moved; the obligation did not.

The U.S. EPA published a technical correction on 5 June 2026 to its rule extending the 2025 Greenhouse Gas Reporting Program deadline to 30 October 2026. Its broader proposal to rescind the program remained pending.

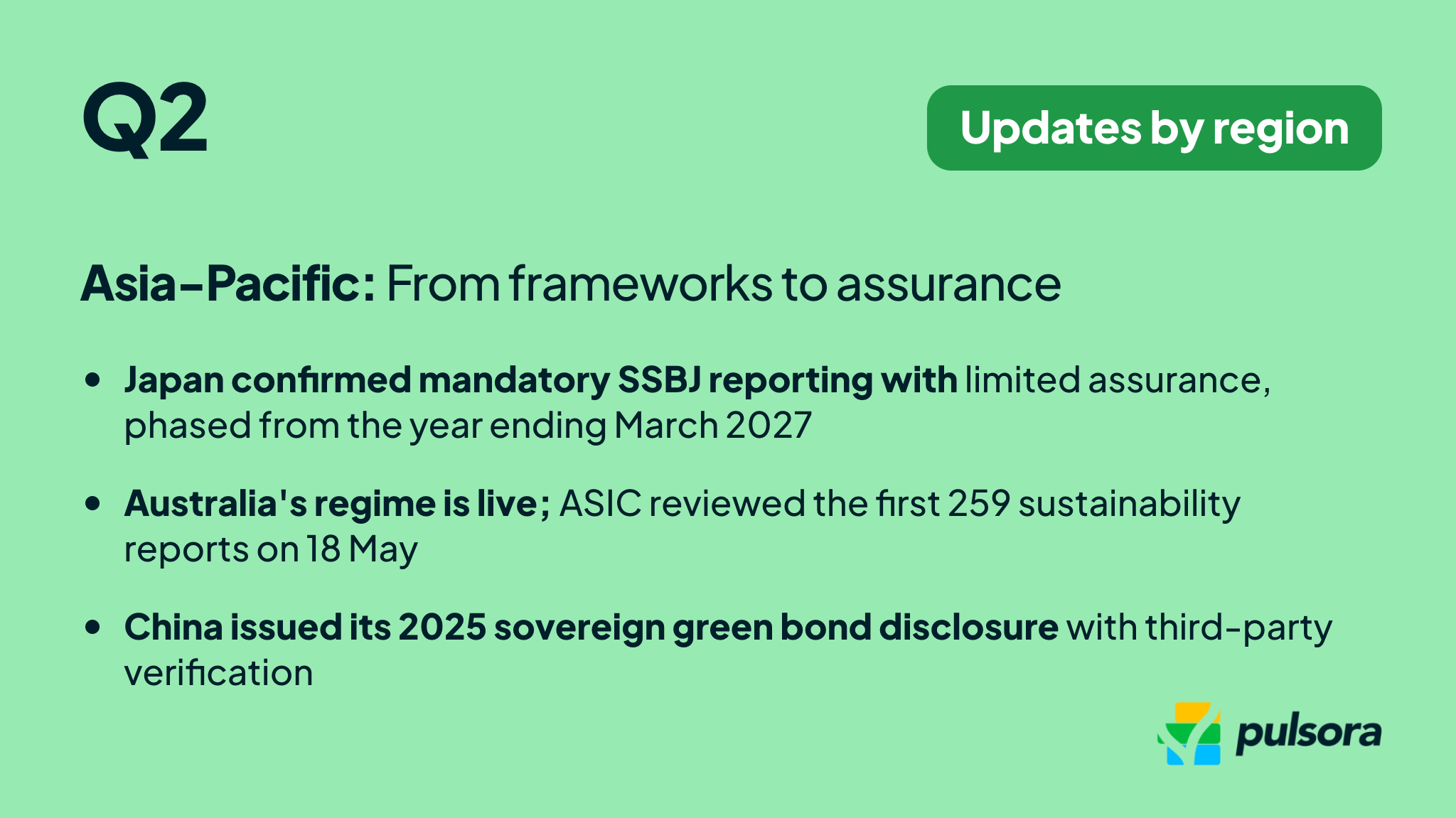

Asia-Pacific

Japan

On 9 April 2026, Japan’s FSA published its final Financial System Council working-group report and roadmap, confirming mandatory application of SSBJ Standards in annual securities reports for TSE Prime companies, phased by market capitalization from the fiscal year ending March 2027, with mandatory limited assurance beginning one year after each phase. Japan’s regime stays functionally aligned with the ISSB global baseline.

Australia

With its mandatory climate-reporting regime now live, ASIC on 18 May 2026 issued early observations from its review of the first sustainability reports lodged under the Corporations Act (259 reports as at 6 May 2026), flagging six improvement areas including misuse of disclaimers and weak climate-risk identification.

China

On 15 May 2026, China’s Ministry of Finance released its 2025 sovereign green bond disclosure, with third-party verification, continuing the build-out of the country’s green-finance infrastructure.

Other regions

UK

On 5 June 2026, the FCA’s quarterly consultation CP26/17 proposed simplifying product-level climate-disclosure requirements in its ESG Sourcebook for asset managers, life insurers, and pension providers, following a post-implementation review.

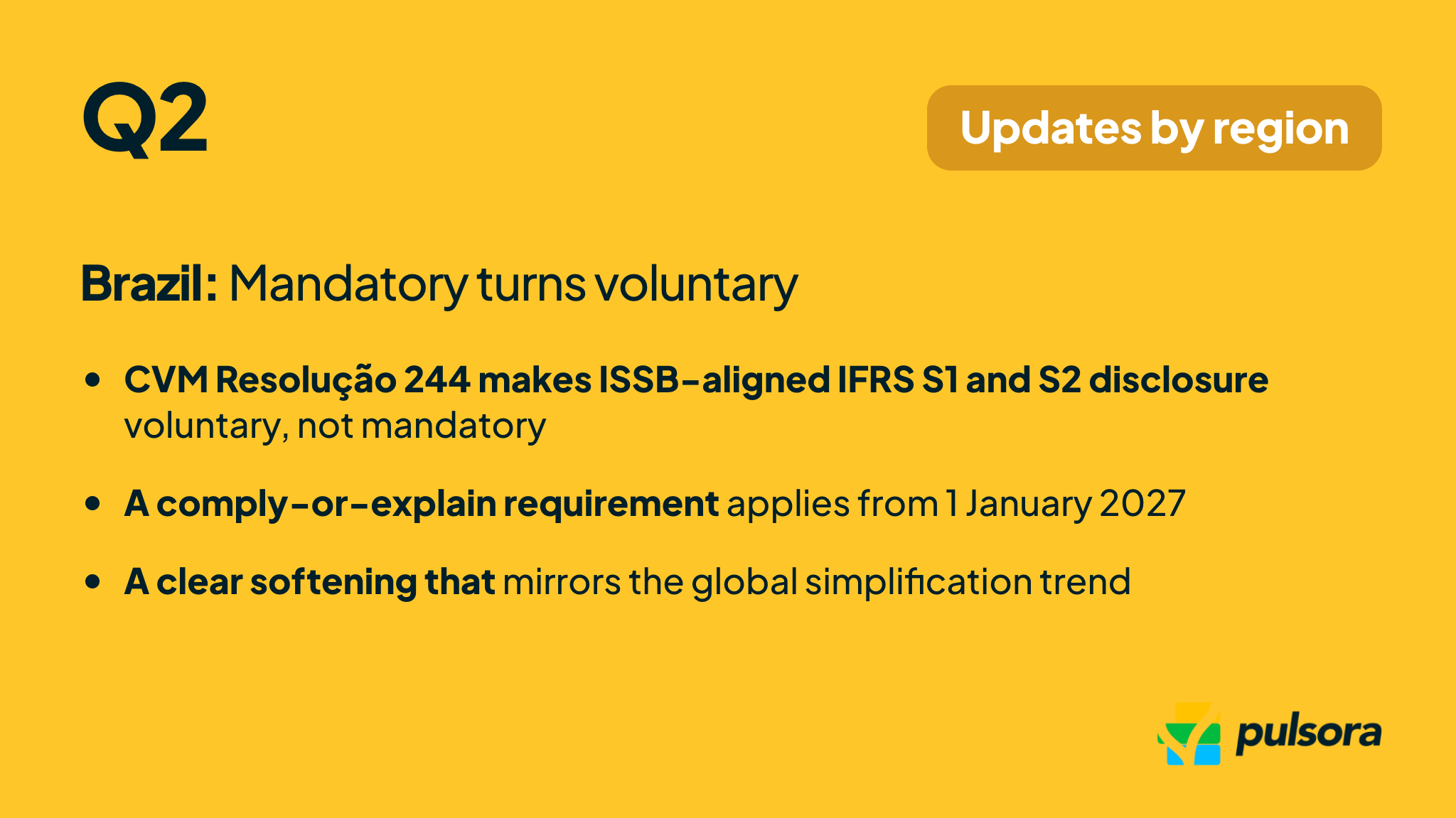

Brazil

On 29 May 2026, Brazil’s securities regulator CVM issued Resolução 244, making ISSB-aligned (IFRS S1 and S2) sustainability disclosure voluntary rather than mandatory for listed companies, with a comply-or-explain requirement from 1 January 2027. It is a notable softening that mirrors the global simplification trend.

Voluntary frameworks updates

Global Reporting Initiative (GRI)

GRI advanced its pollution workstream. A public consultation on three new draft Topic Standards, covering air pollution, soil pollution, and critical incidents, closed on 8 June 2026, with final pollution standards targeted for 2027.

International Sustainability Standards Board (ISSB)

Having moved its nature project into standard-setting, the ISSB agreed at its April and May 2026 meetings to develop nature-related disclosures as an IFRS Practice Statement that supplements IFRS S1 and S2 and draws on the TNFD framework, with an exposure draft targeted for October 2026.

Science Based Targets initiative (SBTi)

On 11 June 2026, SBTi published the final Corporate Net-Zero Standard Version 2.0, its most comprehensive corporate climate framework to date, following two rounds of consultation and pilot testing, with a phased transition for companies setting and revalidating targets.

CDP (Carbon Disclosure Project)

CDP opened its 2026 disclosure cycle, publishing 2026 questionnaires and guidance in spring plus a refreshed scoring methodology, then opening the response window from mid-June 2026. The cycle expands environmental coverage and strengthens alignment with ISSB, ESRS, TNFD, GRI, and SBTN.

SBTN (The Science Based Targets Network)

SBTN’s public consultation on Version 2 of its Step 1 “Assess” and Step 2 “Prioritize” methods closed on 24 April 2026, with consolidated V2 technical guidance planned for mid-2026. Its freshwater V2 pilot runs through the second half of the year.

TNFD (Taskforce on Nature-related Financial Disclosures)

TNFD continued building practical adoption support, releasing a CFO guide on nature-related issues with Accounting for Sustainability on 2 June 2026.

Impact on companies & investors

- Plan for two-speed regulation: Track both the rollbacks (U.S. SEC, Brazil) and the tightening (Australia, Japan, EU assurance), and avoid scaling back capabilities that investors and other jurisdictions still demand.

- Execution beats anticipation: With the first reporting seasons underway, the priority shifts to data systems, controls, and assurance readiness over monitoring new mandates.

- Nature is no longer optional to watch: ISSB, SBTi, GRI, SBTN, and TNFD all advanced nature work in a single quarter. Begin locating your nature-related dependencies and impacts now.

- Simplification is not deregulation: The EU, EBA, and UK framed Q2 changes as burden reduction, not removal. Core disclosure expectations, and rising assurance requirements, remain.

Looking ahead to H2 2026

The second half of 2026 will be dominated by deadlines and adoption. California’s first SB 253 Scope 1 and 2 reports are now expected by 10 November 2026, the EU is expected to formally adopt its revised ESRS, the ISSB’s nature exposure draft is targeted for October, and the U.S. SEC rescission comment period closes in August. For most teams the agenda comes down to three things:

- Meeting the first hard deadlines (California SB 253, plus the ongoing Australian and Japanese phase-ins)

- Preparing for nature-related disclosure (ISSB exposure draft, SBTN V2, TNFD tooling)

- Adapting to finalized simplifications (EU ESRS adoption, EBA, UK product rules)

The throughline into H2 is execution under divergence. As some jurisdictions pare back and others switch on mandatory regimes, companies with resilient data and assurance foundations will navigate the fragmentation best.