Q1 2026 marked a pivotal shift from framework-building to real-world execution in ESG, with direct implications for capital markets, corporate strategy, and financial reporting.

Across regions, the direction of travel is clear but uneven. Europe moved toward simplification without retreat, recalibrating the CSRD/CSDDD regime to ease compliance while maintaining core disclosure expectations. In contrast, the United States saw increasing divergence, with California advancing stringent climate disclosure rules even as federal policy stepped back from climate regulation. Meanwhile, Asia-Pacific markets — particularly China and India — focused on operationalizing existing frameworks, providing implementation guidance and strengthening market infrastructure such as ESG ratings and green finance verification.

At the global level, standard setters and voluntary frameworks are converging on more decision-useful, investor-aligned disclosures. The ISSB’s progression toward nature-related standards, GRI’s continued expansion into biodiversity and pollution, and the scaling adoption of science-based targets all point to a broader shift: ESG is becoming more quantitative, comparable, and financially material.

For financial markets, this quarter reinforced that ESG is no longer just a disclosure exercise. It's increasingly tied to risk pricing, capital allocation, and long-term value creation.

Takeaways for business & finance

- Fragmentation is now a core ESG risk: Companies must navigate diverging regulatory signals—tightening state-level rules (e.g., California) alongside easing federal oversight in the U.S., and evolving but stable frameworks in Europe and Asia.

- From reporting to performance: Regulators and frameworks are pushing beyond narrative disclosures toward measurable metrics (Scope 3, nature, biodiversity, pollution) that directly affect financial outcomes.

- Disclosure = financial infrastructure: ESG reporting is increasingly integrated into financial reporting systems, audit, and governance, requiring the same rigor as traditional financial data.

- Nature is the next climate: With ISSB, GRI, and SBTN all advancing nature-related standards, companies should prepare for biodiversity and ecosystem impacts to become mainstream disclosure topics.

- Global standards, local execution: While ISSB and other frameworks drive convergence, jurisdiction-specific implementation (EU Omnibus, SEBI BRSR, China exchange guidance) will determine actual compliance complexity.

- Investor expectations remain ahead of regulation: Even where regulation softens (e.g., U.S. federal level), investors, lenders, and voluntary frameworks continue to raise the bar, sustaining pressure on companies to act.

- Operational readiness is now critical: Companies need data systems, internal controls, and cross-functional coordination (finance, sustainability, risk) to meet tightening disclosure timelines starting in 2026.

Key regulatory and framework updates by region

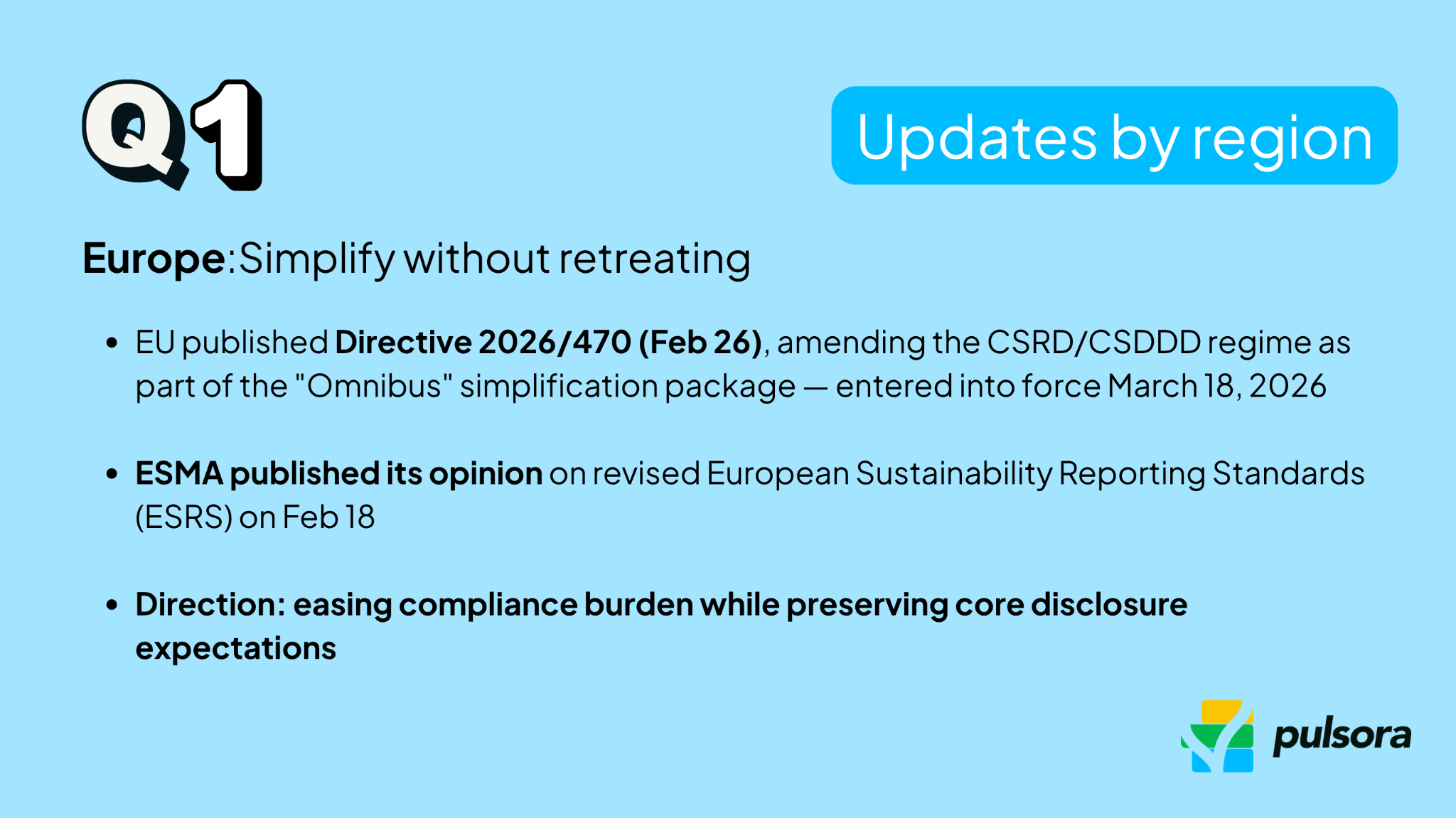

Europe

The EU’s most important Q1 development was the publication of Directive (EU) 2026/470, on 26 February 2026, amending parts of the CSRD and CSDDD regime as part of the sustainability “Omnibus” simplification package. The Commission framed this as reducing reporting burden while preserving core policy goals. The Omnibus amendments entered into force on 18 March 2026, formally reshaping the near-term European sustainability reporting and due-diligence landscape.

On 18 February 2026, the European Securities and Markets Authority (ESMA) also published its opinion on a revised European Sustainability Reporting Standards (ESRS).

North America

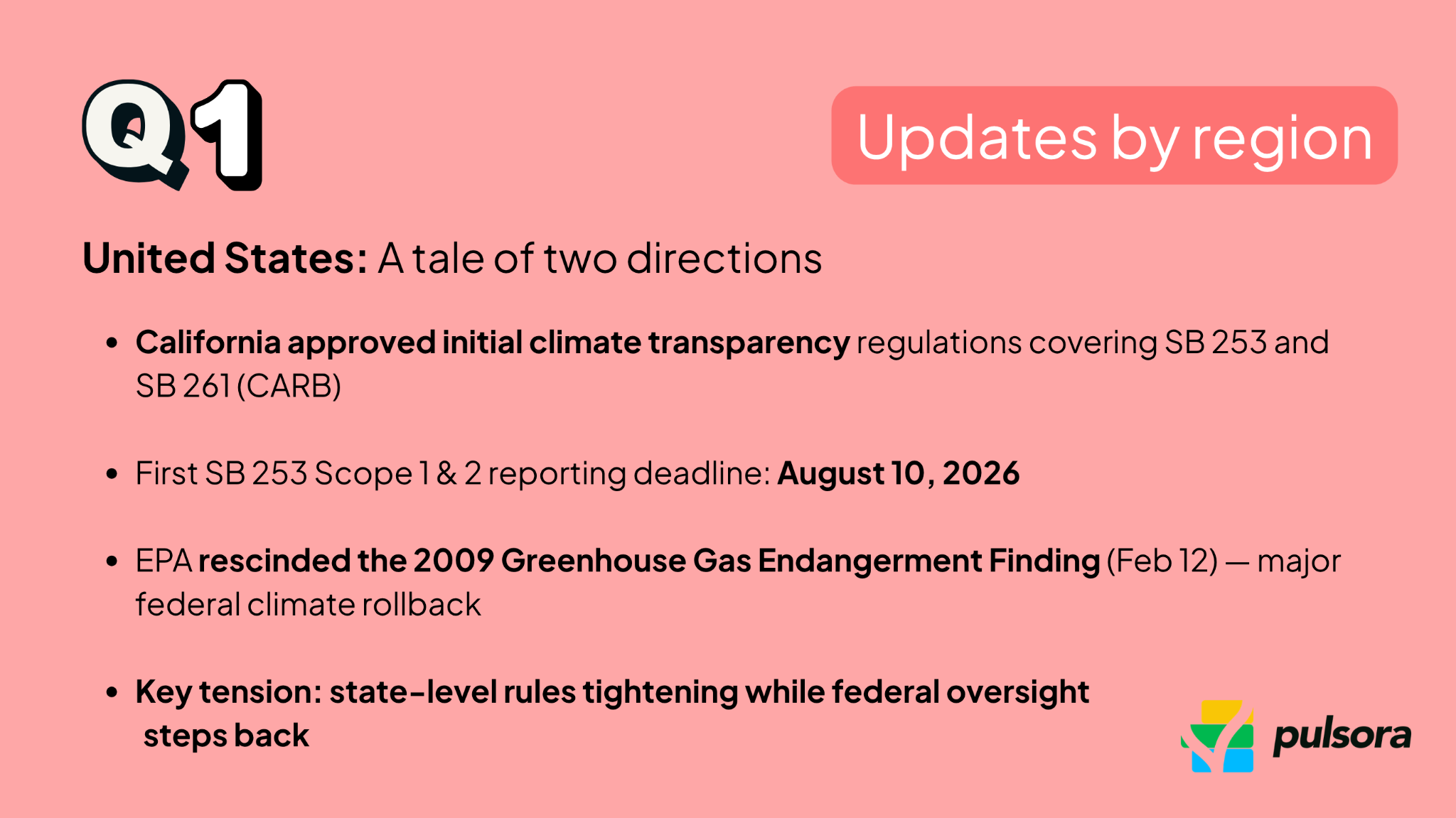

USA

California remained the main U.S. disclosure driver. California Air Resources Board (CARB) approved the initial regulation for California’s climate transparency rules, covering SB 253 and SB 261. CARB’s March workshop materials say the February board action approved key definitions, revenue thresholds, fee structure timing, and a first SB 253 Scope 1 and 2 reporting deadline of 10 August 2026.

Separately, the U.S. EPA finalized its rescission of the 2009 Greenhouse Gas Endangerment Finding on 12 February 2026, a major rollback in federal climate regulation.

Canada

The Canadian Sustainability Standards Board (CSSB) was reappointed to the IFRS Sustainability Standards Advisory Forum on 20 March 2026, reinforcing Canada’s continued role in international sustainability standard-setting. This appointment ensures the CSSB to bring Canadian perspectives to international conversations and stay closely connected to developments shaping global sustainability disclosure standards.

Asia-Pacific

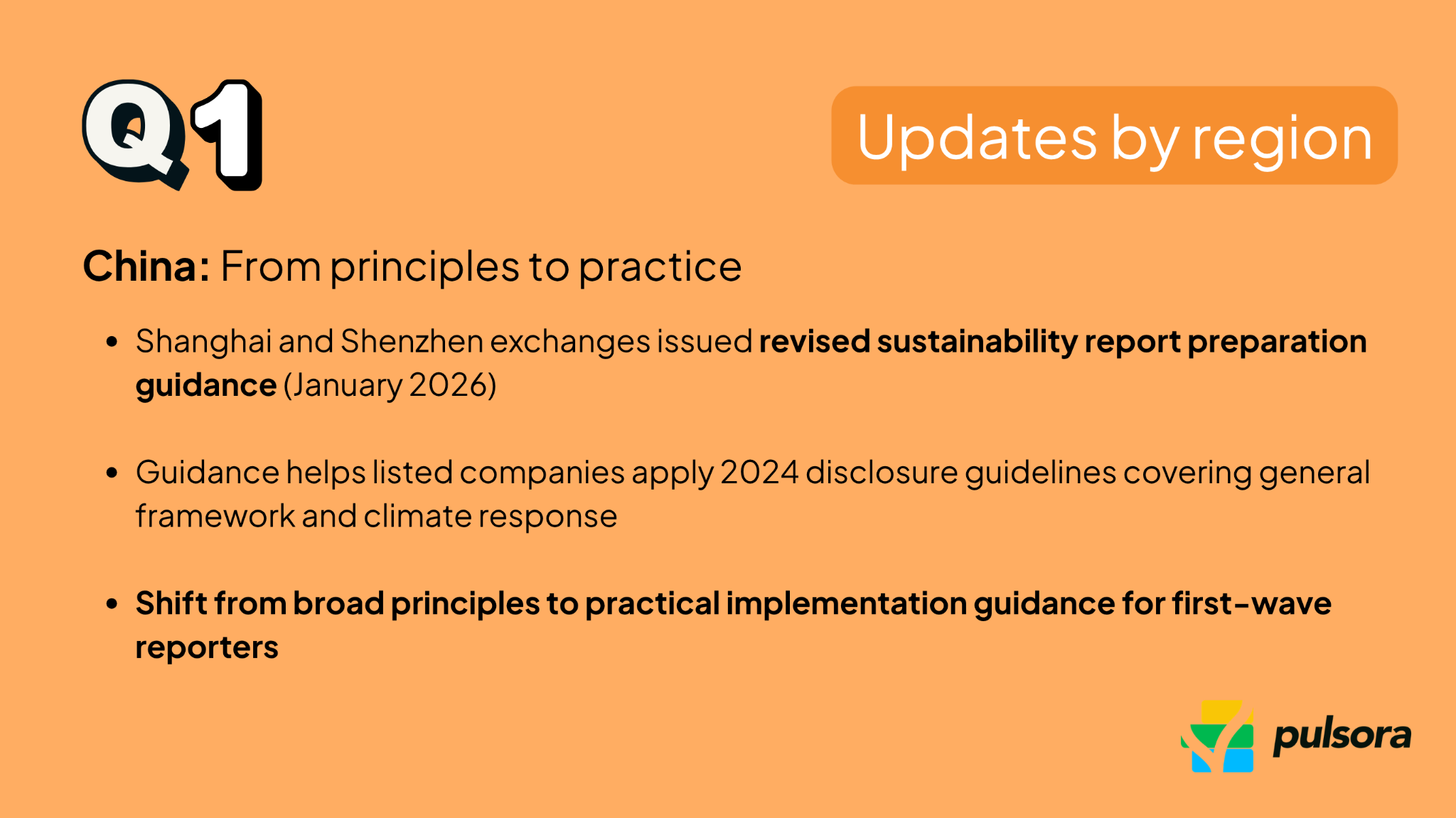

China

China had a concrete Q1 disclosure update: Shanghai and Shenzhen exchanges issued revised sustainability report preparation guidance in January 2026 to help listed companies apply the 2024 sustainability disclosure guidelines to cover the general framework and climate response, and that the regulator will continue improving the sustainability disclosure system.

Q1’s practical implication in China was a shift from broad principles to implementation guidance, especially for first-wave reporters using the exchange guidance.

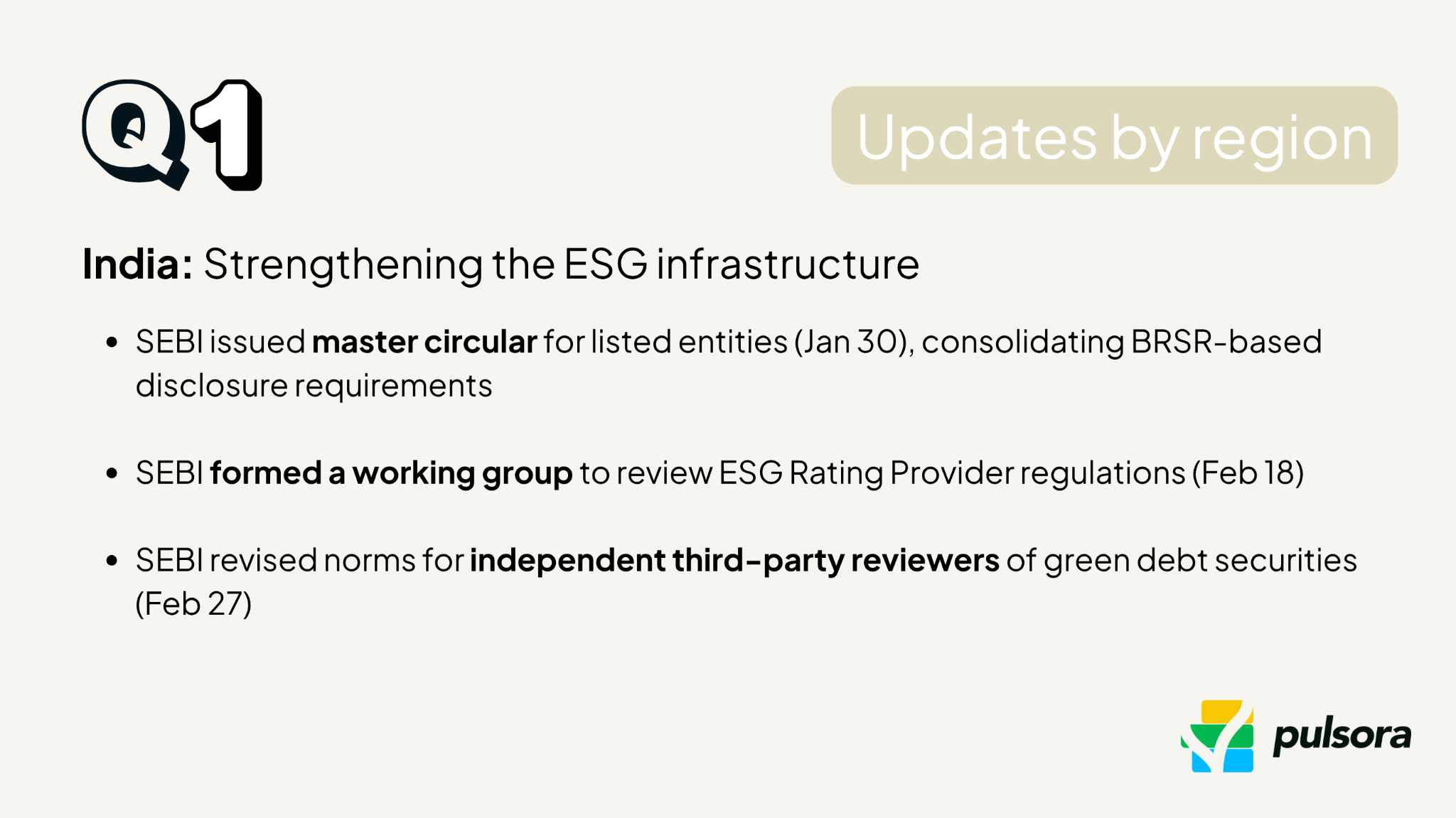

India

SEBI issued its 30 January 2026 master circular for listed entities, which keeps India’s BRSR-based disclosure architecture consolidated in the current compliance package.

SEBI announced a working group to review the regulatory framework for ESG Rating Providers on 18 February 2026, showing continued attention to the quality and reliability of ESG market infrastructure.

SEBI also revised norms for the independent third-party reviewer/certifier for green debt securities on 27 February 2026, aligning review requirements more closely across labeled debt instruments.

Other regions

UK

The Financial Conduct Authority (FCA) opened CP26/5 on 30 January 2026 and closed on 20 March 2026, consulting on aligning listed issuers’ sustainability disclosures with international standards, moving beyond the earlier TCFD-based framework. As a next step, FCA will review the consultation feedback and aim to publish a policy statement in autumn 2026, subject to the final UK SRS, with the rules coming into force from 1 January 2027. The UK government decided to endorse the ISSB standards and issue UK SRS S1 and UK SRS S2 for voluntary use, following consultation in February 2026.

The UK government also published its response on oversight of sustainability assurance, pointing toward a stronger assurance framework.

Voluntary frameworks updates

Global Reporting Initiative (GRI)

On 26 January 2026, GRI said Q1 would focus on a streamlined sustainability reporting system, including consultations on labor and economic-impact standards, while the Biodiversity and Mining Standards took effect from 1 January 2026.

GRI published practical biodiversity support in February, including guidance to help companies improve biodiversity reporting, and continued public consultation on labor standards.

On 30 March 2026, GRI launched consultation on draft standards to strengthen pollution reporting. March also featured continued work on the economic-impact standards project.

International Sustainability Standards Board (ISSB)

In its January 2026 meeting, the ISSB discussed the objective and scope of a project on nature-related risks and opportunities and received implementation feedback on IFRS S1 and IFRS S2 from the Transition Implementation Group.

The March 2026 ISSB update shows that ISSB decided to move the nature-related disclosures project from research to standard-setting in its work plan. The Board tentatively decided to add more detailed disclosure requirements and guidance on nature-related strategy, responses, transition information, and targets.

Science Based Targets initiative (SBTi)

On 22 January 2026, SBTi announced that it had reached a milestone of 10,000 companies with validated targets, signaling continued scale-up of science-based target adoption.

On 3 February 2026, SBTi launched a new public consultation on the updated Automotive Net-Zero Standard draft, reopening consultation after earlier feedback.

On 19 March 2026, SBTi published an updated FLAG Guidance to improve clarity and consistency for companies setting forest, land and agriculture targets.

CDP (Carbon Disclosure Project)

On 25 February 2026, CDP published “Prepare for the 2026 Disclosure Cycle” and its 2026 disclosure hub, signaling the start of the year’s reporting preparation and updated guidance process.

SBTN (The Science Based Targets Network)

On February 10, 2026, The SBTN launched a pilot project for companies to set and validate expanded freshwater targets. SBTN will release Version 2 of its freshwater target‑setting guidance in 2026.

On March 24, 2026, The SBTN opened a public consultation (24 March–17 April 2026) on updated guidance for companies on assessing and prioritizing nature impacts. The consultation focuses on the major updates under consideration for Version 2 of its Step 1 “Assess” and Step 2 “Prioritize” methods, a meaningful technical update for nature target-setting, planned for release mid-2026.

Looking ahead to Q2 2026

For companies and investors, Q2 will be less about new announcements and more about execution readiness:

- Building systems for upcoming reporting deadlines

- Testing data quality and internal controls

- Aligning disclosures with evolving global standards

The key theme going into Q2 is clear: the window for preparation is narrowing, and organizations that move early on data, governance, and cross-functional integration will be better positioned to navigate the increasingly complex ESG landscape.